Executive Summary

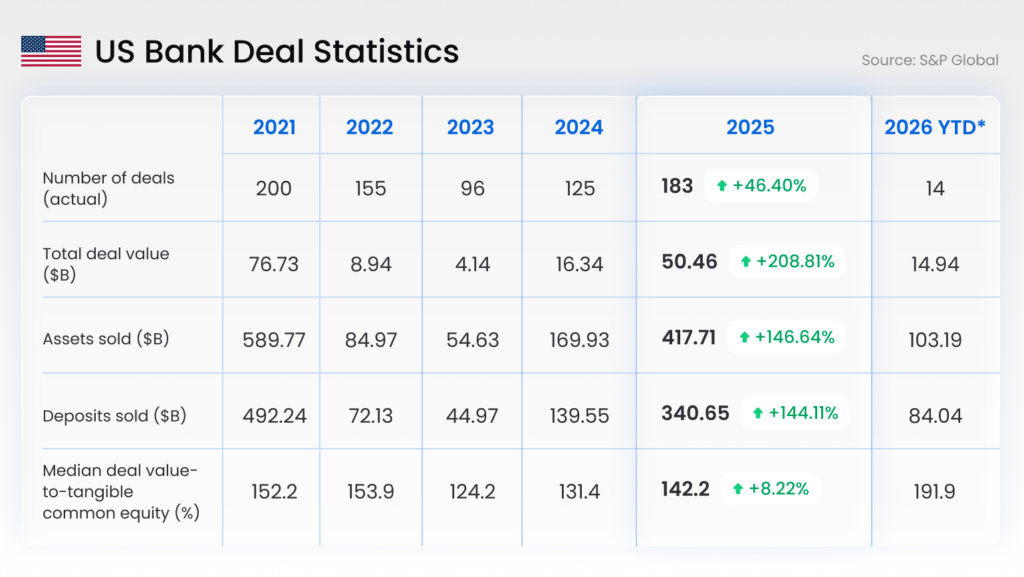

U.S. bank M&A activity has re-accelerated, with 125 deals totaling $16.34 billion in 2024 and continued momentum into 2025 with 183 deals worth $50.46 billion.

On merger announcement day, customers don’t ask about synergies. They ask:

- Will my fees change?

- Will my rate drop?

- Will my app or branch experience break?

In the 30–60 days around integration, deposits move quickly, and competitors know it. 9-12% of retail base deposits are expected to be lost in an M&A event, per industry estimates.

For Heads of Retail Banking, using offers as your shield during M&A can protect any disruption your customers might become frustrated with.

The banks that hold deposits aren’t the ones with the most creative campaigns. They’re the ones that can make and keep a clear value promise across every channel, with end-to-end governance and audit-grade control.

The Environment: Mobile Deposits + M&A Volatility

Deposits are already a high flight risk

As we noted in the Executive Summary, U.S. bank M&A activity is picking up momentum. With 125 deals totaling $16.34 billion, a number that increased in 2025 to over $50.46 billion.

History shows that consolidation creates deposit attrition. Industry estimates suggest that 9–12% of deposits are at flight risk during and shortly after integration, particularly among digitally active and multi-banked households.

Where do those deposits go?

Increasingly, not just to another traditional bank, but to fintech and neobank platforms.

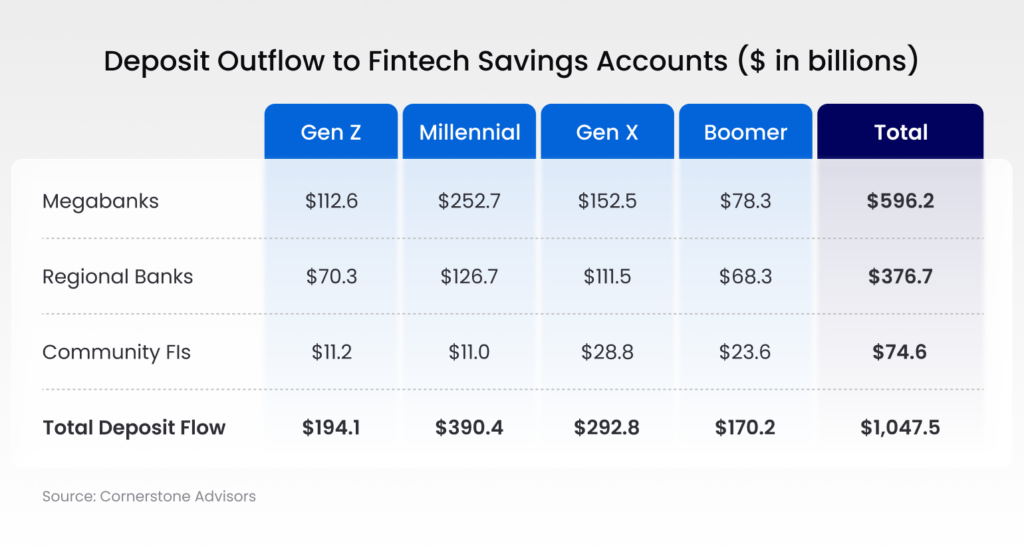

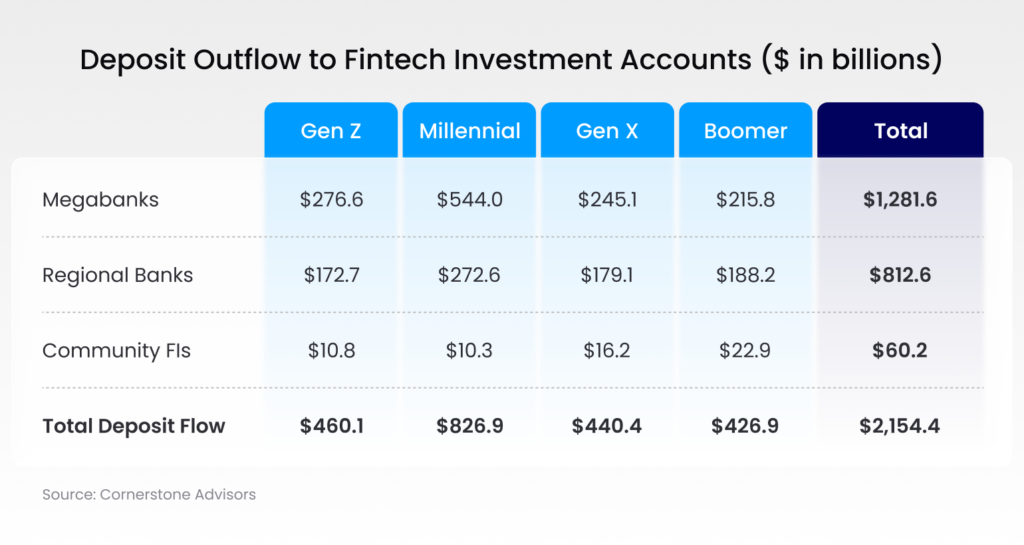

A Cornerstone Advisors report shows that over $3 trillion has shifted from traditional institutions to fintech platforms, including:

- $2.154T to fintech investment accounts

- $1.048T to fintech savings accounts

And this isn’t confined to younger segments. Gen X and Boomers represent a significant share of displaced balances.

Checking has increasingly become a transit point. Funds land and then move to higher-yield savings or investment platforms.

During M&A, that transit time shortens. Uncertainty accelerates movement. Deposits leave faster.

M&A creates a predictable attrition window

Integration introduces friction:

- Product changes

- System cutovers

- Channel disruptions

- Tier or benefit inconsistencies

That friction is enough to trigger relationship re-optimization. Balances consolidate elsewhere. Primacy weakens.

M&A is not only strategic, it is operationally fragile and deposit-sensitive.

The Executive Imperative

So what?

- M&A creates a concentrated deposit flight window.

- Executives must look at their deposit funding mix, and model out a solution to backfill those lost deposits.

- They may choose sources like brokered deposits (which can be expensive), or they can turn to their Offer strategy as an ally to help reduce that deposit runoff.

- Broken or inconsistent offers turn uncertainty into complaints, and complaints into conduct risk.

How Offers Protect Primacy

In this context, offers go beyond campaigns and act as stabilization tools. They allow retail leaders to:

Reaffirm value quickly

The bank can provide concrete answers to uncertainty with retention-oriented offers like:

- Fee freezes or waivers during integration

- Relationship rate boosts tied to balance retention or direct deposit

- Tier status protection through conversion

- Loyalty bonuses for maintaining primary relationships

Executed early and consistently, these reduce perceived risk and discourage deposit migration.

Stabilize balances with precision

Instead of blanket giveaways, banks can deliver targeted, time-bound incentives tied to:

- High-balance households

- Direct deposit relationships

- Multi-product customers

- Tier status or tenure

The objective is precision retention and preventing margin erosion.

Protect trust by honoring promises

Offers and tier benefits are perceived as promises. When eligibility logic differs across channels (or fulfillment breaks), complaints rise. In an M&A window, trust is fragile. Execution failures amplify regulatory and reputational risk.

The Real Differentiator: End-to-End Offer Governance

Most banks can design an offer strategy. Fewer can execute with end-to-end offer governance:

- Controlled lifecycle from eligibility, design, through to enrollment, fulfillment, and retirement

- Clear ownership and approval workflows

- Version control and full auditability

- Suppression, and conflict rules

- Exception handling and reconciliation

- Disclosure alignment and fairness controls

Without this, offers become brittle: weakly governed, slow to launch, inconsistent to deliver, and risky at scale. For a Head of Retail Banking, this means it’s balance sheet protection and conduct control.

The Operating Model Behind It

In an M&A cycle, personalization without governance increases risk.

What’s required is end-to-end governed offer orchestration. One entitlement decision across every channel.

It rests on four capabilities:

- Decisioning

Who gets what, and when — under eligibility and suppression rules. - Fulfillment

Apply benefits consistently across app, contact center, and branch — with reconciliation controls. - Controls

Approvals, disclosures, fairness testing, audit trails, and monitoring. - Measurement

Retention lift, incentive cost, leakage, complaints, and channel consistency.

This is how a value promise becomes operational reality.

The Takeaway

In an M&A cycle, you don’t need more personalization.

You need retention-oriented offers that are reinforced with end-to-end governed offer orchestration: the ability to design, approve, deploy, fulfill, and monitor retention actions under clear policy and financial controls, so customers receive one coherent and consistently honored experience.

Offer orchestration is both a defensive balance-sheet tool during M&A and a growth tactic.

Because when deposits are already mobile, retention is not won with messaging. It is won in execution.