The banking delivery battle over the last decade is shifting to the banking product battle over the next decade.

If there is one stern lesson bank leaders have learned over the past couple of years, it’s how hard it is to organically grow customers (and their deposits especially) in a market that’s getting more competitive by the day. Yet, the current hypercompetitive onslaught can really be dated to about a decade ago when megabanks (like Chase, founded 1877) launched strong mobile banking apps that contributed to a closing of customer satisfaction gaps and organic market share losses against small and midsize banks and credit unions.

For decades prior, strong community financial institutions relied upon, with much less product and marketing emphasis, consistent market share gains against national players like Chase.

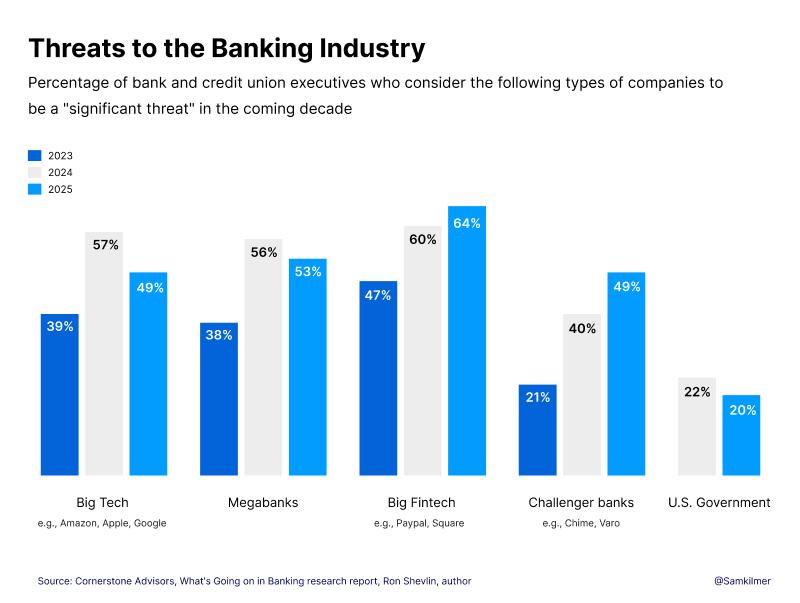

The launch of Apple’s iPhone in 2007 and the proliferation and ubiquity of consumer and business use of Apple and other smartphones over the following decade fundamentally changed banking competitiveness. As Cornerstone Advisors’ What’s Going On in Banking research points out, Big Tech (like Apple Card, launched 2019), Big Fintech (like Square, founded 2009), and challenger banks (like Chime, launched 2014) add significantly to the competitive pressure. All of these strong competitors are predominantly digital in their reach and have quickly grown to become as significant a competitive threat as megabanks.

An interesting story shapes up when looking over a decade of Ron Shevlin’s research within What’s Going On in Banking. In response to these growing digital competitive pressures, banks beefed up their digital delivery capabilities with digital servicing replacements. Then, digital sales technology replacements grew to become the top investment areas, where they have remained in the raging battle over delivery.

Yet, when industry analyst Tristan Green dug into the traits of banks and credit unions that have consistently grown deposits over several consecutive quarters, three traits stood out: aggressive (fast, streamlined) digital account opening delivery, engagement-based rewards checking product, and a focused business banking product suite. That’s one delivery trait and two product traits. That’s no accident. The growing battle is over product.

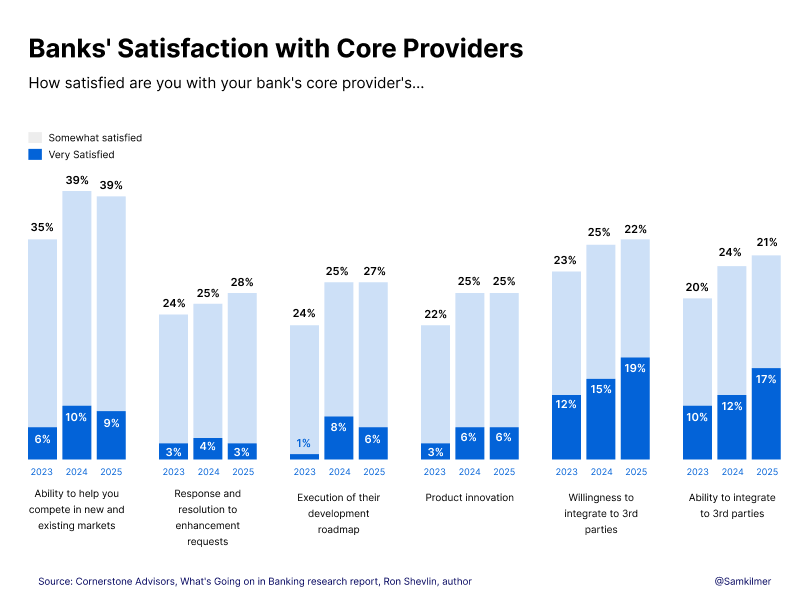

Winning the product battle is difficult for banks. As the What’s Going On in Banking research points out, well under 40% of banks are satisfied with their core provider’s product innovation and ability to help the bank compete. Much like the way many banks turned to a growing list of specialized digital servicing and digital sales systems and providers to fight the delivery battle, they are now looking outside their cores for the ammunition to fight the growing product battle.

As a veteran banker, fintecher, and advisor to banks, credit unions, fintechs, and their investors, I judge that there are three important actions for bank and credit union leaders to win this battle:

- Get hyper efficient to free up and shift resources into product development and outreach to test, learn, and refine products. Better benchmarking and management accounting is required for team accountability because the competitiveness of this market forces self-funded innovations.

- Create new products with differentiating hooks found in the value overlaps that cross the normal banking categories of credit, payments, and deposits (fiduciary or off-balance-sheet investments). That could be as simple as a consumer debit and credit payment product with helpful loyalty nudges or as complex as a commercial bundle of industry-specific C&I loans paired with an industry-specific ERP-integrated treasury solution.

- Grow adoption of the products using compelling outreach like shareable self-help content for consumers and industry-and-integration knowledge for businesses. Even serial bank (vs. organic customer) acquirers will face pressures to improve this competence because it will allow them to win more deals from higher valuations beyond predictable cost takeouts and balance sheet tweaks.

Afterword

It was great to be part of Zafin’s last Banking Leadership Summit in Charlotte and to talk shop with David Ladic and several other industry leaders about shared experiences and possibilities in addressing industry challenges and opportunities.

Sam Kilmer is a Managing Director and leads Cornerstone Advisors’ Research & Fintech Advisory Practice working with fintechs and industry investors. He is a contributor to GonzoBanker and hosts the Fintech Hustle podcast.