A foundational shift in card economics could be underway

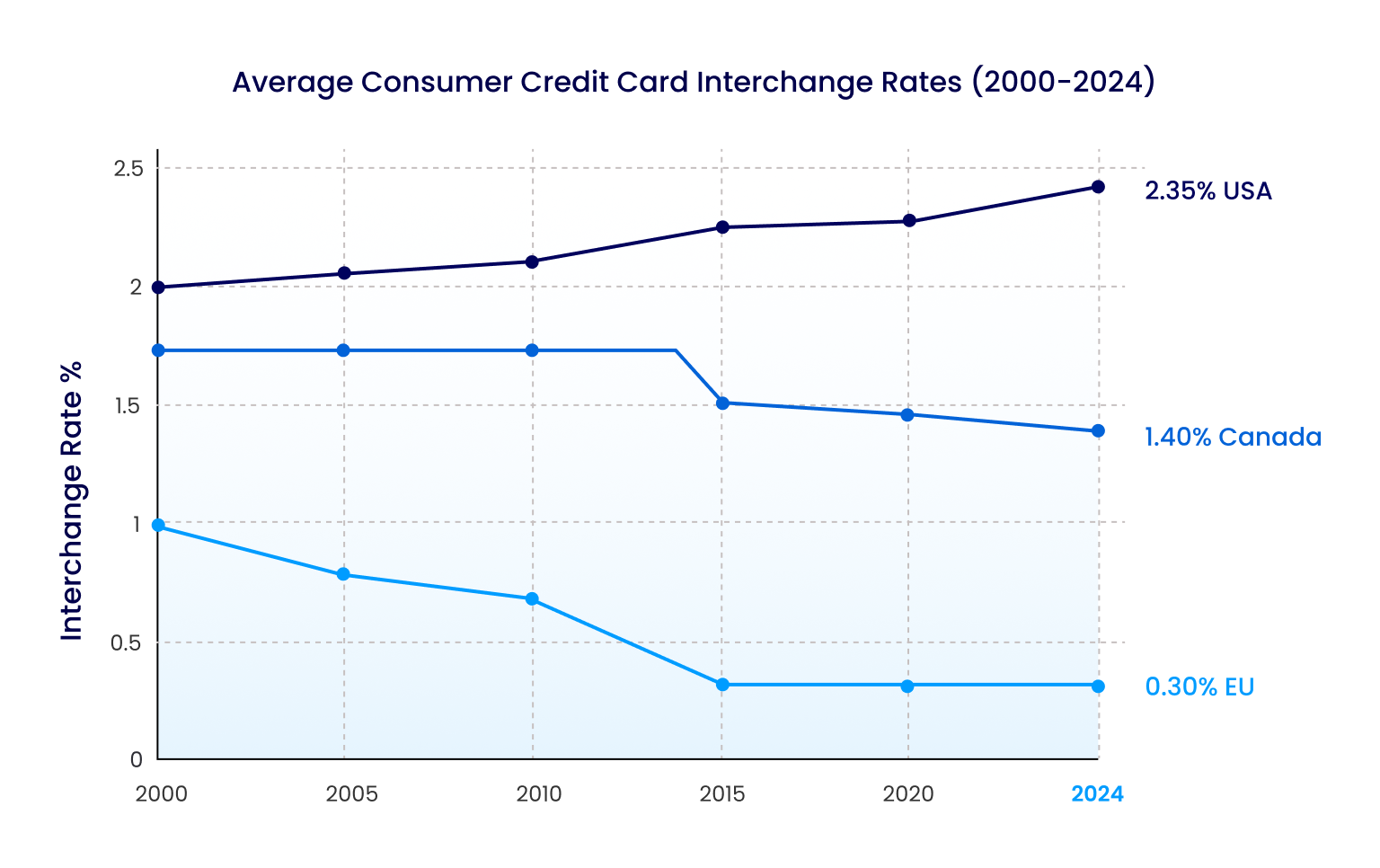

Over the past two decades, credit card interchange fees in the United States have steadily climbed, becoming a significant operating expense, and pain point, for merchants. In 2010, the average interchange rate sat around 2.0%. By 2024, it reached approximately 2.35%

After a 20-year antitrust litigation, Visa and Mastercard have agreed to a proposed settlement that will lower interchange fees by 10 basis points over the next five years, and introduce a 1.25% cap on standard cards.

On the surface, a 10 bps cut might not be a monumental change, but could signal the beginning of a longer term shift towards lower interchange fees (similar to paths we’ve seen in Canada, and more acutely in Europe). This event will have a tangible impact: applied to billions of transactions and distributed unevenly across card tiers, it represents a meaningful shift in card-reward economics, particularly for basic, no-fee, and mass-market cards that depend heavily on interchange to fund their card-specific loyalty offerings.

This change marks a material shift in the economics of loyalty. If your loyalty strategy relies solely on credit card rewards, this is the moment to re-think your strategy or consider how to develop a robust relationship-based loyalty strategy.

What Exactly Happened? Breaking Down the Interchange Settlement

The litigation focused on two main issues:

- Interchange levels charged to merchants, and

- The “honor all cards” rule—requiring merchants to accept all Visa or Mastercard cards, including high-fee premium cards, if they accept any at all.

Under the proposed agreement, average interchange will fall from roughly 2.35% to 2.25%, and the impact will be felt differently depending on the type of card involved.

The most consequential change is the introduction of a hard cap for standard or basic credit cards, which will be limited to 1.25% interchange for the next eight years. This is a meaningful decline from typical rates in the 1.5%–1.8% range. In contrast, premium and rewards cards (often ranging from 2% to 3%) will see smaller proportional reductions and will not face a cap (that does not necessarily mean less impact in this category for consumers).

Another major shift is the potential for merchants to reject premium cards altogether or introduce added surcharges to accept them. While this is less likely to impact large scale retailers, it may influence acceptance among small businesses, much like we see today with AMEX not being as widely accepted as Visa and Mastercard due to higher fees.

How These Changes Will Reshape Card Rewards

The implications for card rewards programs are significant, especially for issuers that rely on interchange to fund points, cash-back, and everyday perks. Basic or no-fee cards will feel the immediate pressure.

When interchange drops from around 1.5% to 1.25%, the economics of funding rewards become stretched. For many issuers, the simplest response will be to reduce or eliminate points, scale back everyday perks, or introduce or increase annual fees for cards that historically had no fees at all, or relatively low annual fees (e.g. $89 per year).

This mirrors what happened in Canada, Australia and the European Union after interchange caps were introduced; annual fees rose, and rewards programs became more conservative almost overnight.

What just happened with credit card interchange fees?

Could this be the first domino for the U.S.?

- U.S. = uncapped, litigation-driven, rewards-heavy

- Canada = voluntary negotiated caps, moderate rewards

- EU = hard regulatory caps, rewards effectively collapsed

No country does premium cards like the U.S.

- Only in the U.S. do premium cards carry a 2–3% interchange

- These cards have created the “richest” card loyalty programs in the world, but ubiquitous acceptance could be impacted.

Could this lead to a continued increase in debit cards?

- 65% of Gen Z report using a debit card at least once per week (often via digital payment and mobile wallets / alternative payment methods).

Premium cards, however, tell a different story. Because they are not subject to the 1.25% cap, this could spur a “barbell” strategy where premium cards grow even more differentiated. Issuers may continue raising annual fees (such as $1,000+ annual fees for top-tier premium cards) and enriching rewards in order to justify those fees. The result could be a more polarized market: basic cards shifting toward utility, and premium cards becoming more exclusive and perk-heavy.

A secondary effect may come from merchants themselves. To avoid paying higher interchange, some may offer small incentives for customers to use lower-fee cards. Over time, this could subtly influence consumer behavior at checkout, nudging spend toward standard cards and away from premium ones. Alternatively, merchants may no longer accept premium cards, or introduce a 2-3% surcharge for using them.

Industry observers are already debating whether this settlement is a precursor to future action on premium interchange. Europe provides precedent that premium cards may eventually be targeted as well, though the length of this litigation—spanning almost two decades—indicates that the path toward further adjustments may not be swift.

Assessing the potential impact across card categories

The first priority is to understand where card rewards are most vulnerable. Basic and no-fee cards deserve immediate attention, followed by an assessment of how premium cards may be affected by changes in merchant acceptance.

From there, banks should begin modeling what a relationship-based loyalty program could look like. This includes tiering based on total value, building bundles that elevate basic cards into broader product packages, and refreshing premium offerings so they continue to justify higher fees.

A “barbell” strategy, reinforcing premium cards while modernizing basic cards as part of broader account relationships, can help banks navigate this transition smoothly. Expanding or launching customer value tiers is a powerful way to anchor this strategy.

| Card Category | Typical 2024 Interchange | Impact Under Settlement | Potential Card Loyalty and Rewards Outcome |

|---|---|---|---|

| 1. Premium and Co-Brand Cards (Visa Infinite, World Elite, Airline/Hotel/Retail Co-brands) | ~2.0 to 3.0% | Not capped, but newly vulnerable. Merchants may reject them or surcharge up to 3%. Co-brands heavily exposed because partners rely on interchange to fund points. |

|

| 2. Mass-Market Rewards Cards (Signature, World, everyday cashback) | ~1.5 to 2.0% | Capped at 1.25%, largest profit compression |

|

| 3. Basic and No-Rewards Consumer Cards | ~1.0 to 1.3% | Already near 1.25% cap, small operational changes |

|

| 4. Small Business and Commercial Cards | ~1.8 to 2.8% | Not capped, but merchants may reject corporate cards due to high fees |

|

The Bigger Picture: A Turning Point for Loyalty Strategy

For U.S. banks, interchange fees have long been a reliable engine to fund the richest card rewards market in the world. A typical card with a 2.20% interchange rate might allocate up to 1.7% toward rewards, with the remainder covering fraud, operations, and issuer margin. When that revenue source compresses, the sustainability of these programs is called into question.

Where a Typical Credit-Card Interchange Fee Goes

(Example: A $100 credit-card purchase with ~2.20% interchange = $2.20 total)

Total Interchange: $2.20

This flows from the merchant → acquirer → issuer, and is distributed roughly as follows:

Issuing Bank (≈ 70–90% of the interchange)

$1.60 – $2.00 goes to the card-issuing bank (Chase, Citi, Amex issuing division, etc.)

This funds:

- Rewards funding (usually the biggest slice)

- Fraud losses & chargebacks

- Credit risk / loan loss reserves

- Customer service & operations

- Issuer margin

Typical internal breakdown inside the issuer’s share:

| Component | Approx. Share of Each Interchange Dollar |

|---|---|

| Rewards (points, miles, cashback) | 40%–70% |

| Fraud + chargeback expenses | 10%–20% |

| Borrowing costs & credit losses | 5%–15% |

| Operations & servicing | 5%–15% |

| Issuer profit margin | 5%–15% |

Interchange profit is only one way card issuers make money as the primary profit engine interest income from revolving balances. Because issuing banks will likely maintain their interchange profit, the decrease is likely to come from the ‘rewards’ bucket.

This settlement accelerates an industry shift that was already underway: loyalty cannot remain a single-product strategy. Banks with loyalty programs built exclusively around credit card transactions are disproportionately exposed. As interchange decreases, card-based loyalty becomes both less profitable and less effective as a tool for deepening customer relationships.

The Path Forward: From Points to “Whole Customer Loyalty”

The solution is not to eliminate rewards, but to evolve them, shifting from a card-centric model to a holistic framework that recognizes the entire customer relationship. Leading institutions are already taking this approach, rewarding customers not just for credit card spend but for their total relationship and set of affiliated activities.

This includes deposit balances, mortgage and loan relationships, debit and credit transactions, household relationships, engagement habits, and meaningful behaviors such as digital adoption or securing accounts with multi-factor authentication. This creates opportunities for banks to deliver more relevant, consistent, and true win-win loyalty experiences so customers reap additional value the more they with the institution.

Crucially, this also expands the value banks can offer customers without relying solely on income from credit interchange. Fee waivers, preferred rates, bundled benefits, personalized offers, and micro behavioral incentives can now sit alongside traditional rewards to create a more modern and flexible loyalty ecosystem.

Banks like U.S. Bank, RBC, SoFi, Revolut and others, are already exploring these models to deliver holistic loyalty and insulate their offering from shifting market conditions like decreasing interchange fees; strengthening customer engagement and turning a regulatory shift into a strategic advantage.

What Financial Institution Should Do Now

If you haven’t started down this path, now is the time to move beyond single product, credit card-centric loyalty and build programs that reflect the full relationship a customer has with the institution. Build the program in a layer that is decoupled from core banking systems to enable dynamic products, tiers, campaigns and benefits that unify products across the customer lifecycle, recognizing total value, not just credit card spend.

By adopting a whole customer retention approach, banks can create loyalty program to grow depth of products and drive customer retentionin a declining interchange environment.

Reduced card interchange revenues might be the wake-up call, but the winning strategy remains the same: recognize the entire customer relationship, and stay competitive regardless of what macro industry shifts occur moving forward.

Turning Pressure Into Advantage

The interchange settlement represents more than a technical adjustment to fee structures.

Banks that respond proactively—not just by adjusting rewards, but by embracing whole-customer loyalty—will be well-positioned to deepen relationships, protect revenue, and differentiate in an increasingly competitive market. Those that remain tied to credit-card-only loyalty models will find themselves constrained, cutting back rewards and losing engagement as economics tighten.

The banks that thrive in this new environment will be those that see beyond the credit card and build loyalty around the full scope of the customer relationship.