Executive Summary

To compete with the growing threat of neobanks and FinTechs, banks often turn to offers and incentives to reduce that customer churn. They design offers that reward customers for their loyalty, strengthen customer relationships, and expand their share of wallet.

Let’s look at how Zafin’s suite of capabilities work together as part of an integrated platform to unlock end-to-end offer management, enabling banks to:

- Configure and launch offers rapidly with less dependency on core systems or IT resources

- Create compliant disclosures tied directly to offer logic using modular, reusable components with Zafin AI

- Automate fulfillment and rewards with rules-based monitoring

- Continuously monitor enrollment, fulfillment, and customer behavior to support compliance, auditability, and actionable insights

The outcome: Faster market execution, stronger compliance, reduced operational overhead, and more tailored customer experiences – all with less reliance on core systems or IT resources.

Why do banks take so long to launch new offers?

Fragmented Offer & Disclosure Ownership

“3–4 teams were making independent edits to the same offer disclosure.” – said a senior banker in North America.

Offers are configured and fulfilled in product or campaign tools, while banking disclosures live elsewhere in disjointed or siloed document repositories. There’s no single platform tying them together, risking the rise in conflicting updates sent to customers.

Manual Disclosure Creation

“The process usually takes about 3 months…a lot of the delay is legal, risk, and compliance reviews”– said a senior banker in North America.

Each customer engagement channel requires its own disclosure variant. With each disclosure being created and managed manually as separate documents, the process can take months to coordinate. This becomes a huge bottleneck as it increases operational overheads and risks inconsistencies or manual formatting errors.

No Automation for Offer Expiry

Most banks still use spreadsheets to track offer end/expire date which requires constant manual monitoring. In case of any oversight, banks run the risk of displaying expired offers on their bank’s customer-facing channels, exposing regulatory gaps and damaging customer trust.

No Visibility into Disclosure History

“We can’t trace what was shown to the customer at onboarding.”– said a senior banker in North America.

Since offers and disclosures aren’t linked, banks can’t guarantee that the disclosures a customer sees always matches the current offer terms. This makes dispute resolution nearly impossible, impacting customer experience and trust while raising servicing costs. It also makes audit trails difficult, significantly increasing compliance risk.

On average, 70% of disclosure update steps remain manual, typically taking banks 100+ days to launch even a basic offer-driven campaign.

How does Zafin solve this?

Let’s start with a real-world example.

Imagine a bank’s Marketing, Product, and/or Customer Acquisition/Growth teams aiming to engage existing customers by launching a 6-month long ‘Cash Bonus Offer using New Money’ campaign. The objective is to encourage customers to increase their savings account balances by depositing new funds not already held at the bank.

Offer Details:

Target Customers: Existing customers who are part of the bank’s Bronze tier and currently hold a High-Interest Savings Account (HISA).

Reward: Customers who fulfill these conditions qualify to receive a $500 cash bonus credited directly to their HISA.

Step 1: Offer Enrollment

The banks’ Marketing, Product, and/or Customer Acquisition/Growth teams construct the offer together without relying on core systems or IT resources. Using Zafin’s Propositions capability, they configure the offer across three core components:

Eligibility

Which banking customers and/or accounts are eligible for this offer. In this case:

- Customer holds certain products (a HISA)

- Customer segment or cohort (the Bronze tier)

Other available criteria:

- Bank employee status

- Restrict number of enrollments

- Any Custom Attribute – String, Number, Decimal, Date, Boolean

- Account was never held before Offer StartDate or between X Date and Start Offer Date

- Account is jointly held

- Customer has payroll account

- Customer age

- Customer is part of a household

- Customer opened on or after a date

Action

What behavior do we want our customer to exhibit to become eligible for the offer. In this case:

- Customer brings in net new money (tracking the customers’ combined balance across all their product holdings within the bank, either as a “daily closing balance” or an “average closing balance” at end of the month).

Other available criteria:

- Minimum, Combined, Average Balances

- Balance Increase

- Number of Transactions (with minimum Value)

- Transaction Filters: Codes, Channel

- Customer Segment, Cohort

- Customer Relationship Tier

- Account Region, Branch Account Enrolled in Offer, Household Offer

Reward

What rewards would eligible customers receive once they demonstrate the desired behavior. In this case:

- Cash bonus (a $500 cash bonus credited directly to their HISA).

Other available reward structures: :

- Cash Back

- Fee Waiver

- Bonus Interest

- Loyalty Points

- Free Merchandise

- Select payout in account based on balance, account age

- Payout when $X of reward is accumulated

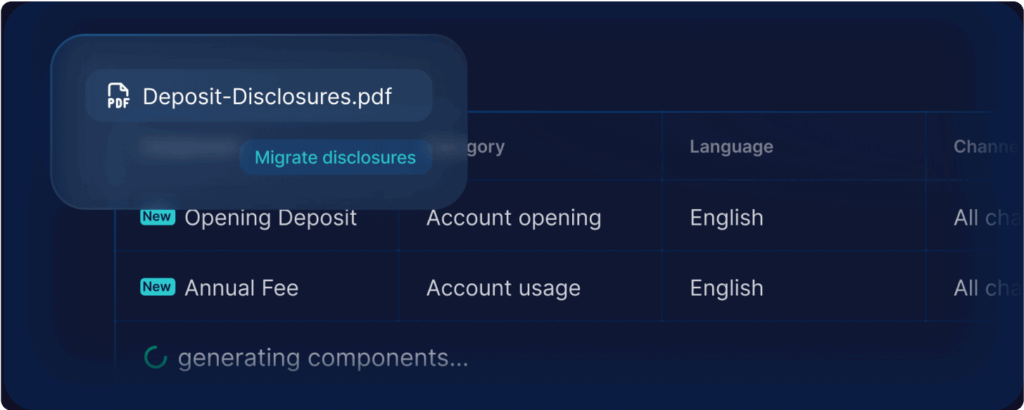

Speeding up Disclosure creation

Zafin’s Disclosures capability lets banks create disclosures from variable, modular components linked directly with Propositions. It allows teams to ingest offer variables and create a library of disclosures components and sets via an intuitive disclosure builder, making the process quick and error-free. Templates for the 3 core components – Eligibility, Action, and Reward – are especially valuable, since banks can create an offer using any combination of them.

If the bank has run a similar net new money offer previously, then the disclosure creation process is even quicker by leveraging Zafin AI. It can ingest prior disclosures and transform them into modular, reusable building blocks to quickly reuse for this offer.

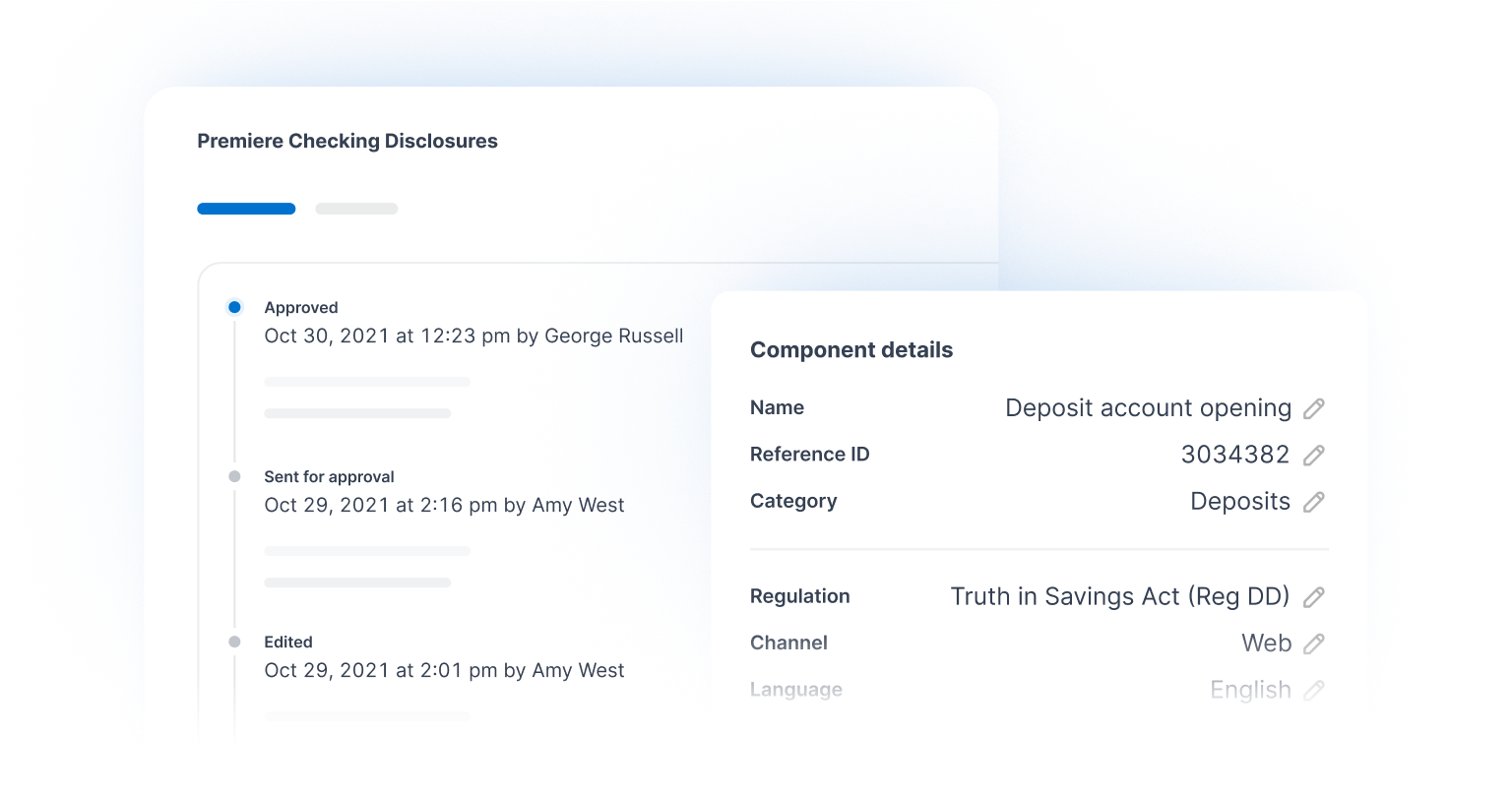

Disclosures also has compliance and governance built in. It connects to jurisdiction-specific regulations for smarter compliance tracking, ensuring that every disclosure created is compliant with governing regulations. It also provides a configurable, multi-level, rule-based approval workflows – ensuring that every disclosure created is fully traceable and audit-ready at any point.

Surfacing the correct disclosures across all marketing channels

Zafin is an official Adobe Solution Partner. This allows the Disclosures capability to integrate seamlessly with Adobe’s entire suite of MarTech products including Workfront, Asset Manager, Journey Optimizer, and more.

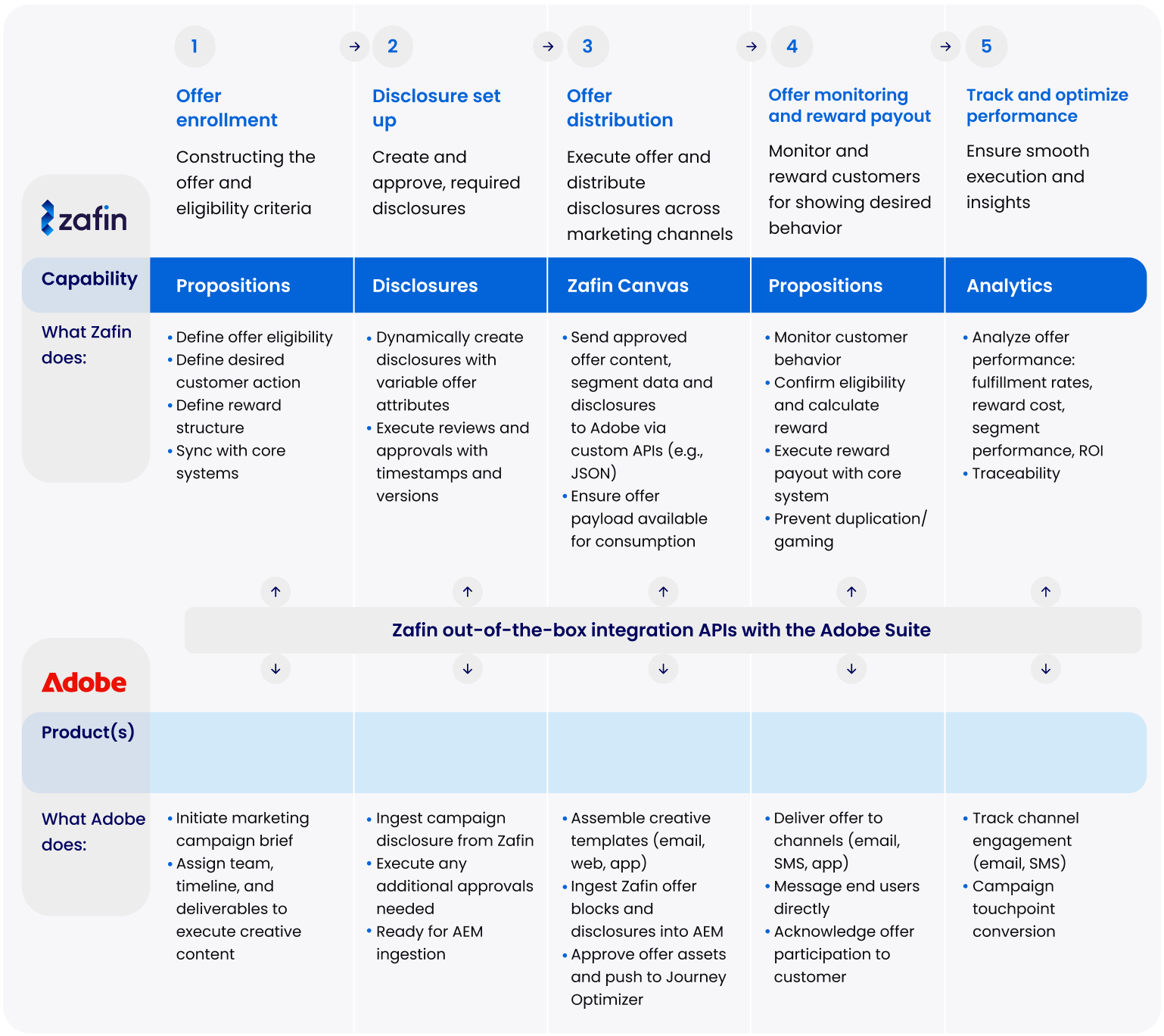

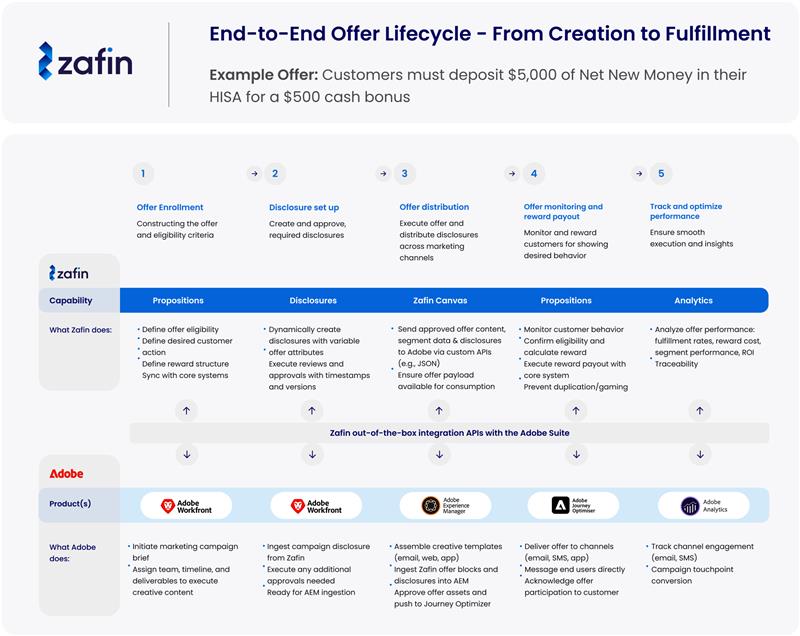

End-to-End Offer Lifecycle - From Creation to Fulfillment

Example Offer: Customers must deposit $5,000 of Net New Money in their HISA for a $500 cash bonus

Constructing the offer and eligibility criteria

Create and approve, required disclosures

Execute offer and distribute disclosures across marketing channels

Monitor and reward customers for showing desired behavior

Ensure smooth execution and insights

Capability

What Zafin does:

Define offer eligibility

Define desired customer action

Define reward structure

Sync with core systems

Dynamically create disclosures with variable offer attributes

Execute reviews and approvals with timestamps and versions

Send approved offer content, segment data and disclosuresto Adobe via custom APIs (e.g., JSON)

Ensure offer payload available for consumption

Monitor customer behavior

Confirm eligibility and calculate reward

Execute reward payout with core system

Prevent duplication/ gaming

Analyze offer performance: fulfillment rates, reward cost, segment performance, ROI

Traceability

Product(s)

")

")

")

What Adobe does:

Initiate marketing campaign brief creative content

Assign team, timeline, and deliverables to execute creative content

Ingest campaign disclosure from Zafin

Execute any additional approvals needed

Ready for AEM ingestion

Assemble creative templates (email, web, app)

Ingest Zafin offer blocks and disclosures into AEM

Approve offer assets and push to Journey Optimizer

Deliver offer to channels (email, SMS, app)

Message end users directly

Acknowledge offer participation to customer

Track channel engagement (email, SMS)

Campaign touchpoint conversion

{kind=link}

The integration is enabled by an out-of-the-box, plug-and-play connector for Adobe, delivered through Zafin Canvas – a low-code, intuitive pipeline builder within Zafin IO. This makes it possible for business teams to configure disclosure workflows, with less reliance on IT resources.

Zafin is also built to integrate with the platforms banks already use. If the bank uses other MarTech tools, or has built its own internal tools, Disclosures can also easily integrate with them via API pipelines built within Zafin IO and compliantly distribute disclosures across all channels. This eliminates the need of new vendor onboarding or any change management processes.

Step 2: Reward Monitoring

Once enrollment is complete, the offer goes live and Propositions monitors customer behavior to ensure reward criteria are met.

All reward conditions include a start and end date/open-ended monitoring. In this example, the condition is triggered once the bank observes a $5,000 net new funds increase in the customer’s HISA, held for 90 days.

Step 3: Reward Calculation

When monitoring is complete, Propositions calculates the customer’s reward. In this example, the customer qualifies to receive $500 directly in their HISA for bringing in net new money into the bank.

Step 4: Reward Payout

When Propositions finalizes the reward amount, it deposits the funds directly into the eligible customer’s HISA.

Throughout the Cash Bonus Offer campaign, the platform maintains full audit trails of customer disclosures, approvals, and offer engagement. Once the campaign ends, the system automatically removes offers and reverts disclosures, ensuring full compliance without manual intervention.

Throughout the Cash Bonus Offer campaign, the platform maintains full audit trails of customer disclosures, approvals, and offer engagement. Once the campaign ends, the system automatically removes offers and reverts disclosures, ensuring full compliance without manual intervention.

Throughout the lifecycle, tracking the offer’s performance (i.e. its fulfillment rate, cost of rewards to the bank, total net new money, segment performance, and more) is available in Zafin’s Analytics capability. It syncs with the Propositions capability, ensuring not just a smooth end-to-end offer execution but also detailed insights into its performance.

Conclusion

Time-bound offers are critical for modern banks, but only if executed with speed, precision, and compliance.

Zafin’s unified platform brings together the essential building blocks to make end-to-end offer management a reality:

- Propositions to configure targeted offers

- Disclosures to ensure compliant messaging at scale

- Zafin IO’s connectors to integrate with the bank’s existing MarTech or compliance systems

- Analytics to track and optimize offer performance

Instead of the industry-standard 100+ days required by most banks to launch a basic campaign, Zafin helps the bank go from ideation to execution in days. This enables the Marketing Tech/Ops, Product, Customer Acquisition/Growth teams with faster market responsiveness, and helps Compliance teams ensure every offer is confidently delivered — fully governed, transparent, and auditable.

We’re already working with leading banks globally to modernize their offer management and speed up time-to-market, resulting in increased agility, enhanced customer experiences, and scalable compliance.

Ready to launch your next compliant offer faster? Let’s talk.