Banking has never stood still. Periods of expansion have fueled prosperity. Downturns have shaken entire markets. Rates have shifted and regulations have tightened. Branches have given way to digital experiences, and customer expectations have heightened.

Yet through it all, one constant endured: banks remained at the center of financial gravity – the trusted anchor of financial relationships. Today, that center is shifting.

The rise of the platform economy is redefining where and how value is created. Finance is no longer a destination, but is embedded in the moments that shape life and business.

For the first time in modern banking history, the gravitational pull of customer relationships is moving away from the bank itself.

This change represents not decline, but opportunity – a chance for banks to connect their greatest strengths of trust, scale, and institutional credibility to the digital platforms where customers already live and transact.

Relevance accrues to whoever delivers the outcome, not necessarily the institution with the charter.

The Shift from Universal Banking to the Platform Economy

This evolution goes beyond the technological. It signals a fundamental shift to where value is created: from institutions that owned products to platforms that orchestrate outcomes. This transformation is visible across all segments. In consumer markets, fintechs are leading the way: Chime for deposits, Venmo for payments, Wise for cross-border transfers, and Robinhood for investing. In business banking, platforms such as Toast, Jane, Ramp, and Brex embed payments, cards, and credit directly into software. Providers like Stripe and Adyen integrate acquiring, issuing, and treasury into digital workflows.

Banks still power the regulated rails of deposits, lending, and settlement, but the customer relationship and data increasingly belong to the platforms that own the experience.

Finance has moved from a destination to being embedded in the customer journey. Transactions once conducted in branches now occur in apps, marketplaces, and conversations. Search and advice are now delivered through conversational and agentic AI, while payments flow invisibly through ERP, commerce, and procurement systems.

Relevance accrues to whoever delivers the outcome, not necessarily the institution with the charter. Consider Uber, which holds driver earnings in digital wallets that can be spent or transferred without ever touching a traditional bank. Or Starbucks, where customers preload billions of dollars in balances that function like deposits. These platforms don’t just facilitate payments; they own the experience and control the data.

This marks a new era of growth for those ready to lead. Banks that use their existing endowments of trust, scale, and institutional credibility to orchestrate customer outcomes across connected digital networks will remain central to financial life. Those that don’t, risk being relegated to the background of someone else’s platform.

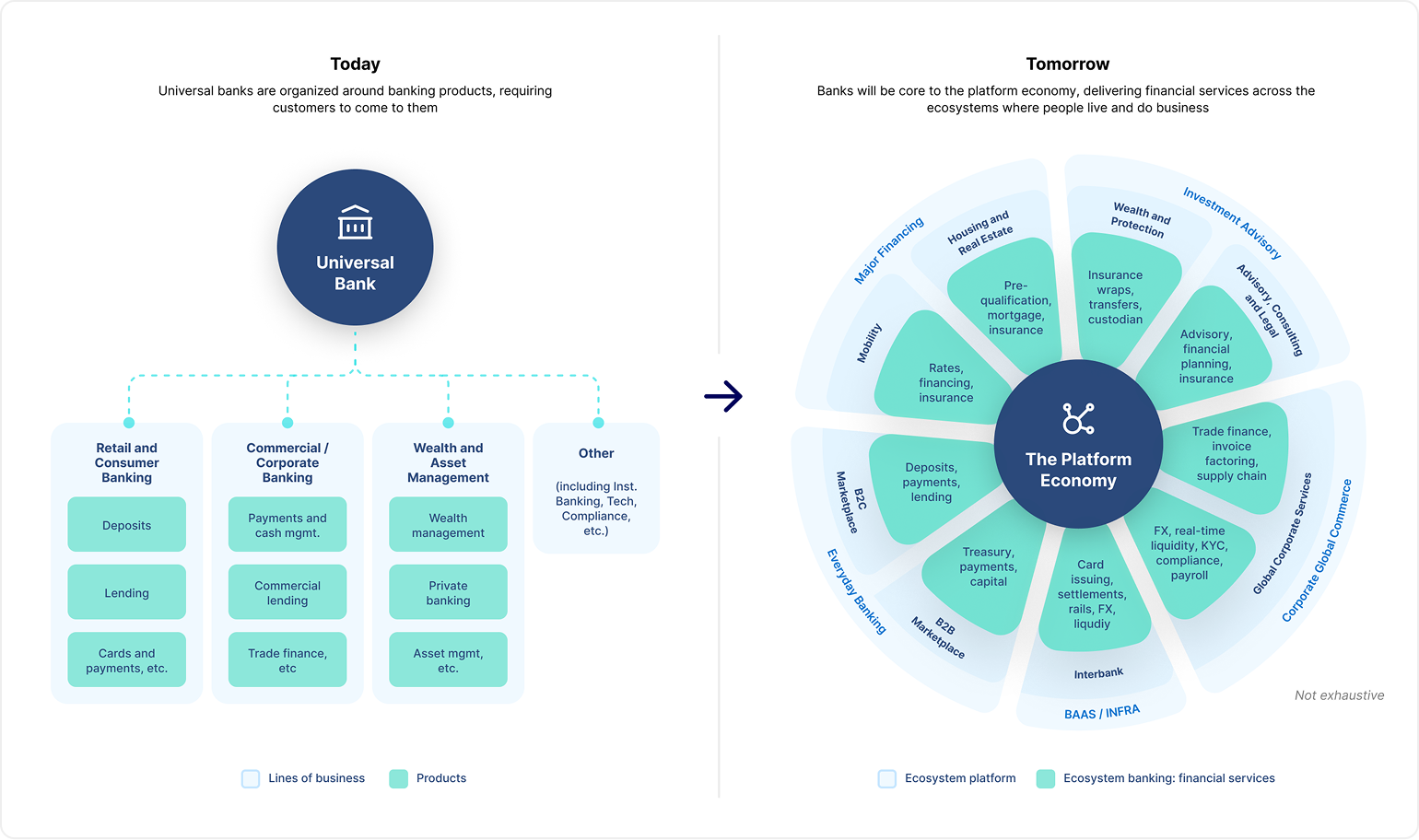

This transformation can be visualized as a structural shift from internal product silos to network-based orchestration.

Today, universal banks are organized around lines of business — deposits, lending, payments, and wealth — requiring customers to come to them. Tomorrow, banks will distribute these same capabilities across digital platforms, embedding financial services where people live and do business.

Ecosystem Banking in the Platform Economy: Where Value and Connection Converge

Ecosystem banking is how banks use their scale and trust to create and capture value within the platform economy. It integrates financial capabilities directly into the commerce, lifestyle, and enterprise platforms where customers already live and work.

Customers no longer need to “go to the bank”; the bank now goes to them — appearing directly within the digital experiences, workflows, and decisions that define modern life.

Banks can participate along a spectrum: from unseen, white-labeled infrastructure providers, to branded, prominent partners, and ultimately to operators of full platforms.

- White-labeled infrastructure providers power services behind the scenes; customers may not even know it’s a bank in the mix.

- Branded partners offer visible, integrated services within external platforms.

- Platform owners combine financial services and customer experience under one roof.

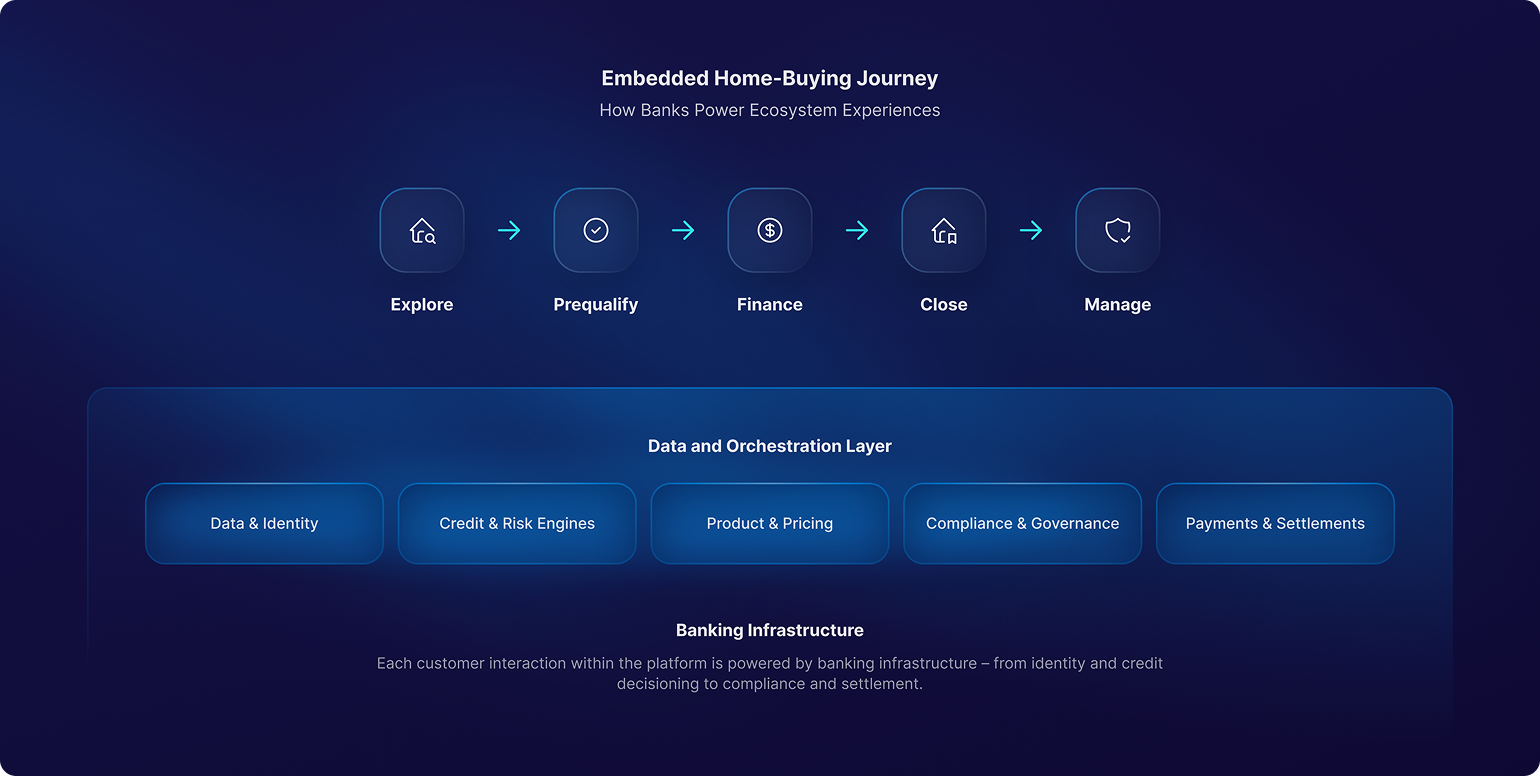

Consider the journey of a customer searching for a home. They begin on a real estate platform, exploring neighborhoods and listings, and connecting with real estate professionals. Before the first home viewing, the platform offers embedded tools, powered by partner banks, to prequalify for financing, estimate monthly payments, and compare rates in real time. When they find a home and make an offer, the mortgage application is initiated within the same platform, using secure data-sharing with the bank’s underwriting systems.

Once the offer is accepted, insurance, title, and closing services are automatically coordinated through the same interface. Post-purchase, the homeowner can view their mortgage, insurance, and home services all in one place, without ever logging into a separate banking portal.

The customer never leaves the platform, yet every financial step, planning, financing, insuring, and payment, is powered by the bank. This is ecosystem banking in action: the platform drives the experience; the bank delivers the compliance, credit, and scale that make it possible.

Competing in the Platform Economy

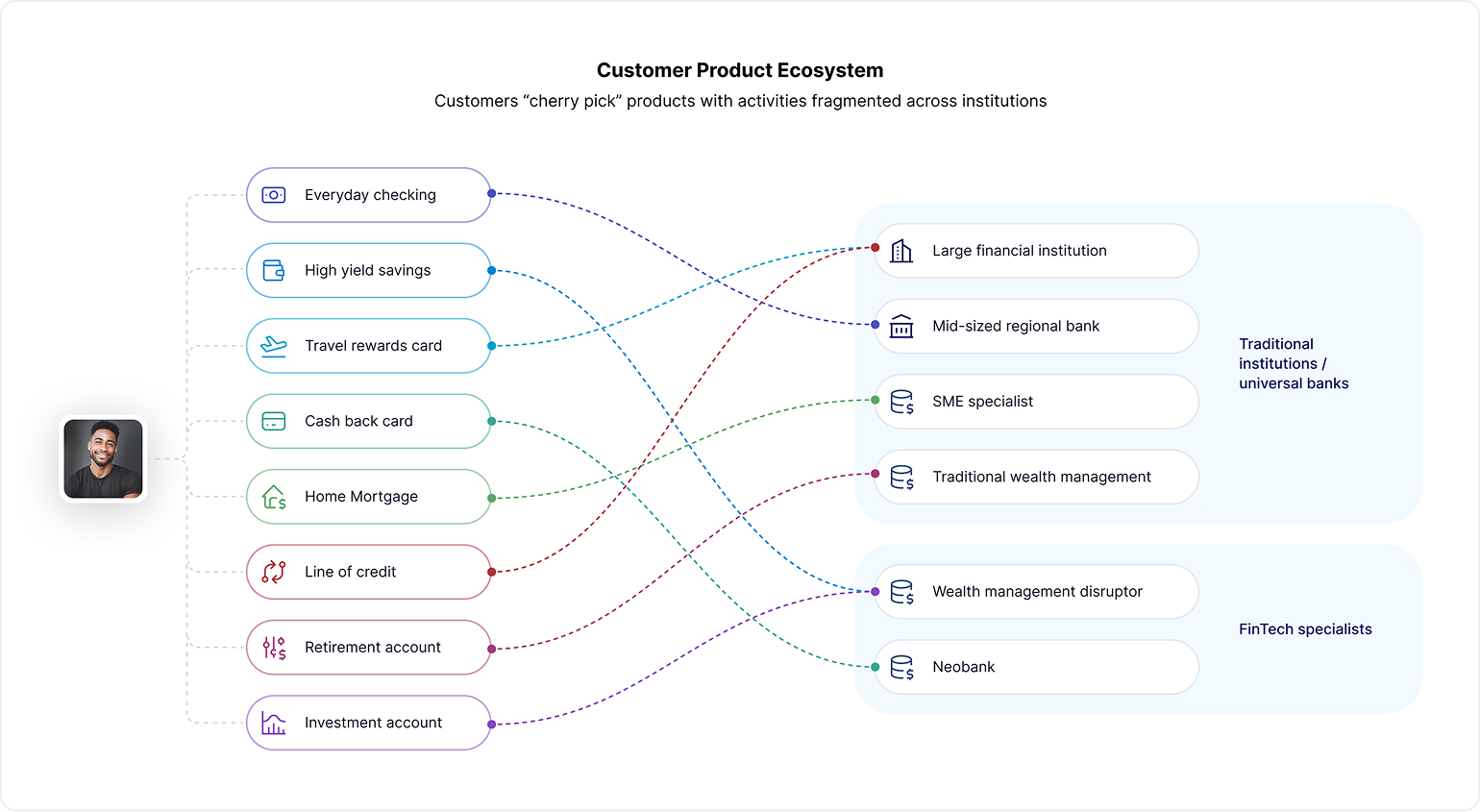

Within the platform economy, competition is no longer defined by product portfolios but by participation. Loyalty is fragmenting. Customers now build their own financial stacks, one app, one outcome at a time. Banks must meet them where they are, or risk becoming irrelevant. Of the typical six products a customer holds, only three are with their primary bank. The rest are distributed across fintechs, regional institutions, and niche providers — a reflection of how loyalty has fragmented across the ecosystem.

Fragmented loyalty in a multi-platform world

The universal bank model, once built on lifetime relationships, has given way to product-by-product competition. Customers now “cherry pick,” choosing institutions and platforms that best meet specific needs rather than relying on a single provider.

This fragmentation reflects a fundamental change in how loyalty forms and fades. As ecosystems expand, customers no longer evaluate banks holistically; they evaluate experiences individually. Winning one product no longer means winning the customer.

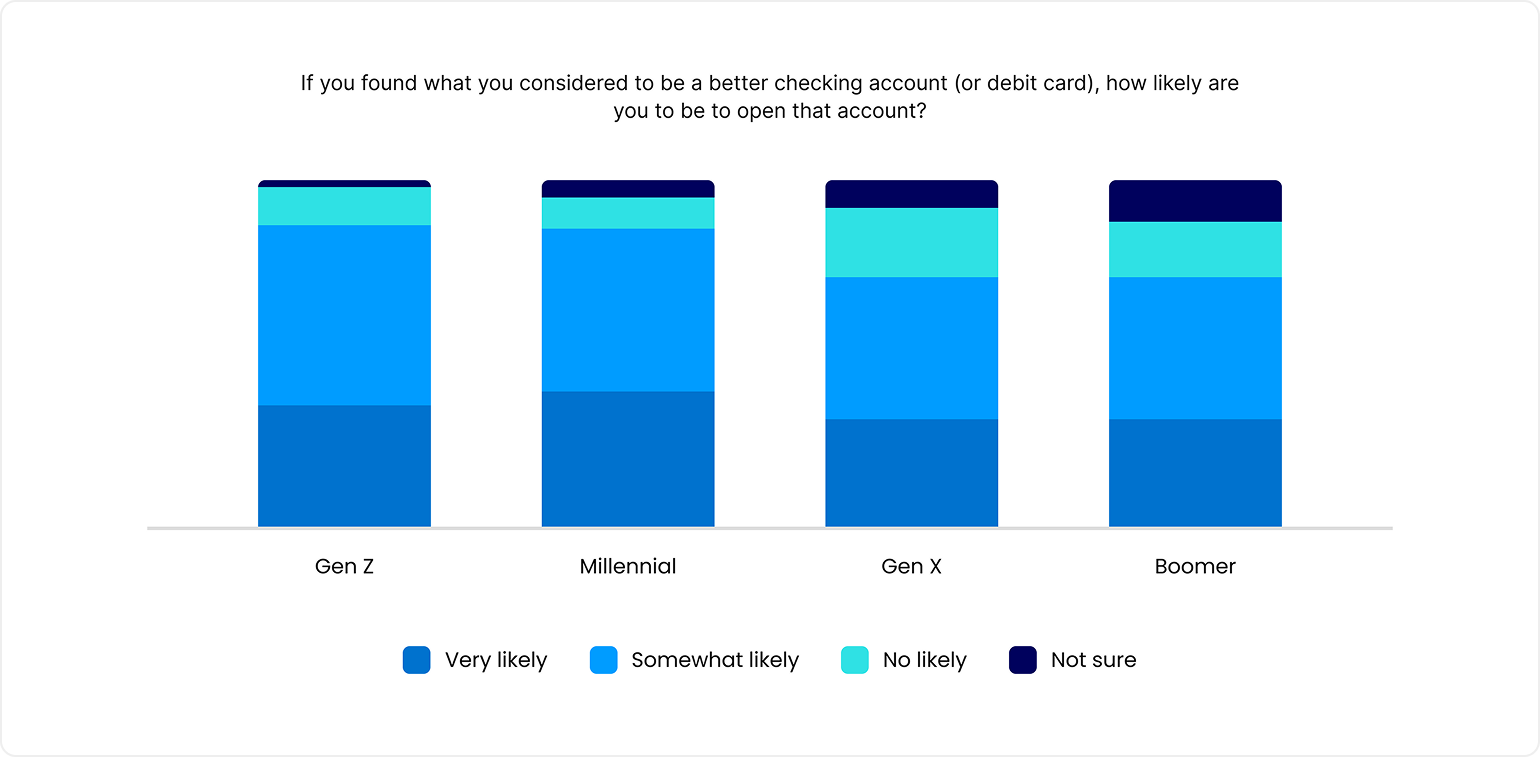

Generational shifts in trust and switching

Younger generations, especially Gen Z and Millennials, show the highest willingness to switch banks or open new accounts when a better experience or offer presents itself. Platforms have trained them to expect instant gratification and seamless onboarding.

With one-click account setup, embedded payments, and automated journeys, the historical barriers to switching — paperwork, branch visits, waiting periods — have vanished. Convenience, not legacy, now determines loyalty.

The implication is clear: holding the account no longer guarantees holding the relationship.

Implications for banks

Customers can now setup recurring payments, split bills, send money internationally, or finance purchases, all without entering a branch or ever logging into their bank’s app. Apple Pay, Venmo, Google Wallet, Amazon, and even TikTok are increasingly handling, storing and moving money in the customer ecosystem user flow – often without customers realizing which institution is powering the financial action. By owning the interface and removing complexity, platforms create a sense of loyalty through convenience, not through financial products alone.

The implication is clear: holding the account no longer guarantees holding the relationship.

In business banking, the shift is even more pronounced. Finance now lives within the systems where work happens – ERPs, commerce platforms, and vertical software. Accounts, payments, issuing, FX, and working capital are embedded directly in daily workflows. Payables and receivables are managed within procurement and billing systems. Treasury services have become programmable, accessed through APIs and files rather than portals. The result mirrors consumer behaviour: holding an account no longer guarantees holding the relationship.

Some banks are already adapting. On defense, they raise switching costs with enterprise-wide loyalty (Bank of America Preferred Rewards; U.S. Bank Smart Rewards), deliver integrated purchase journeys (Commonwealth Bank Home-in; DBS Marketplace), and pursue super app breadth (PrivatBank Privat24). On offense, JPMorgan is redefining data economics by pricing aggregator access to customer-permissioned data in its agreement with Plaid — shifting data access from a free utility to paid infrastructure.

As traditional advantages collapse, banks can still capitalize on strengths that platforms and fintechs cannot replicate:

- Scale, to serve as financial infrastructure across markets and ecosystems

- Trust, to underpin transparency, compliance, and governance across every touchpoint.

Success now depends on how effectively banks extend those strengths into new channels, not by controlling the experience but by powering it. To do so, banks must ensure their products remain discoverable within digital ecosystems and AI-driven environments, where algorithms, not interfaces, increasingly determine relevance.

Trust and Scale: The Endowments That Differentiate

Scale anchors banks at the center of finance

Scale allows banks to remain at the center of finance. As platforms move closer to the customer experience, banks hold the deposits, manage the risk, and process the transactions that power the economy. Where platforms scale users, banks scale balance sheets. Where fintechs optimize experiences, banks optimize resilience and compliance. This makes banks indispensable facilitators, ensuring every payment through a digital wallet, every balance in an app, and every loan from a marketplace is processed, safeguarded, and cleared.

Scale extends beyond transactions to the networks banks create. By linking customers, businesses, governments, and institutions into integrated financial systems, banks expand the participants who can interact and transact. Every additional connection reduces friction, increases opportunity, and accelerates value creation. Scale enables banks to extend network effects beyond the customer-to-customer connections that platforms create, spanning institutions, markets, and industries to deliver outcomes no single platform can orchestrate.

For example, when Stripe Treasury or Shopify Balance offer business banking features, they do so by partnering with regulated banks such as Goldman Sachs and Fifth Third. The platform owns the interface and experience, but the underlying deposits, payment rails, and compliance stack are bank-powered. The bank’s scale and licensing support the ecosystem quietly from behind the scenes, ensuring funds are held, cleared, and protected.

Together, trust and scale allow banks to play roles that no platform or fintech can replicate.

Trust underpins the platform economy

Banks hold the licenses, compliance infrastructure, and history of safeguarding deposits that define what is safe and reliable in the financial system. They ensure loans are backed by liquidity, verify customer identities through KYC standards, and secure payments while protecting against fraud. They provide the compliance framework that enables secure commerce. Where platforms may own the interface, banks supply the assurance that regulators demand and the market depends on.

As a result, banks serve as the foundation of trust for platforms and fintechs. They provide the assurance regulators require for platforms to flourish. They establish the financial legitimacy that strengthens platform credibility. By embedding governance, compliance, and transparency into platform operations, banks project their trust advantage into ecosystems, enabling confidence that platforms cannot create on their own.

For example, large banks such as HSBC, Citi, and JPMorgan facilitate complex cross-border transactions for multinational corporations, managing FX risk, liquidity, and settlement across dozens of countries. Platforms such as Amazon or Shopify may provide merchant services, but when it comes to global treasury and ensuring funds move compliantly through regulated corridors, it is the banks that sit beneath and connect the dots. Banks have established the global trust to manage billions in daily flows, maintain regulatory relationships in every jurisdiction, and absorb risk fintechs struggle to manage today.

Together, trust and scale allow banks to play roles that no platform or fintech can replicate. They anchor transparency and stability while enabling growth across networks. These endowments give banks both the credibility and capacity to operate as financial infrastructure for the platform economy, not just as participants within it.

Translating Endowments into Outcomes

Competing effectively in the platform economy requires more than recognizing scale and trust as banking advantages. It requires converting them into strategic differentiators. Scale must be translated into experiences that deliver outcomes customers value, and trust must be extended into platforms and partnerships through governance that ensures transparency and compliance across every channel.

From recognition to execution

Delivering outcomes in the platform economy follows a simple progression: start with customers, extend through partners, and operationalize through governance. Each stage builds on the last, translating trust and scale into measurable value:

- 1Customer-obsessed culture When a customer applies for a mortgage, they are not buying a loan; they are buying a home. This is where ecosystem banking becomes tangible. Banks can orchestrate complete solutions such as financial planning for budgeting, mortgages for financing, insurance for protection, and security for peace of mind. By curating solutions across products and partners into a single relationship, banks transform their scale advantage into customer relevance through seamless, end-to-end experiences. Relevance begins with outcomes, not products. The ability to recognize customers in real time, deliver on promises transparently, and provide recourse when expectations fall short turns trust into tangible loyalty.

- 2Value-driven partnerships No single bank can deliver every outcome alone. Each institution must decide which outcomes to own based on its franchise strengths, strategic segments, and brand promise. From there, the bank can assemble an ecosystem of partners to fill capability gaps, extending its reach without diluting control. To scale this model, collaboration must become industrialized. Commercials, SLAs, consent, liability, resilience, and onboarding should be standardized so partners can connect consistently. A unified customer experience and shared success metrics make the ecosystem function as one system of value. As the bank moves from selling products to orchestrating outcomes, the “outcome portfolio” should evolve as dynamically as a product roadmap. For example, a retail bank might partner with an energy provider to offer green-home financing, or with a payroll platform to deliver early-wage access.

- 3Orchestration and governance Orchestration and governance ensure these partnerships operate with safety and consistency at scale. Every customer interaction and partner transaction must be governed automatically, not reviewed after the fact. Governance should be built into the infrastructure, not layered on top. This means compliance logic must be integrated directly into product configuration, pricing decisions, and partner interactions rather than layering it on afterward. It also requires centralizing agreement and compliance data at the point of distribution to ensure every interaction flows through the appropriate governance controls. The outcome is assurance that travels with the service, turning governance into an enabler of innovation rather than a constraint.

The Infrastructure Imperative

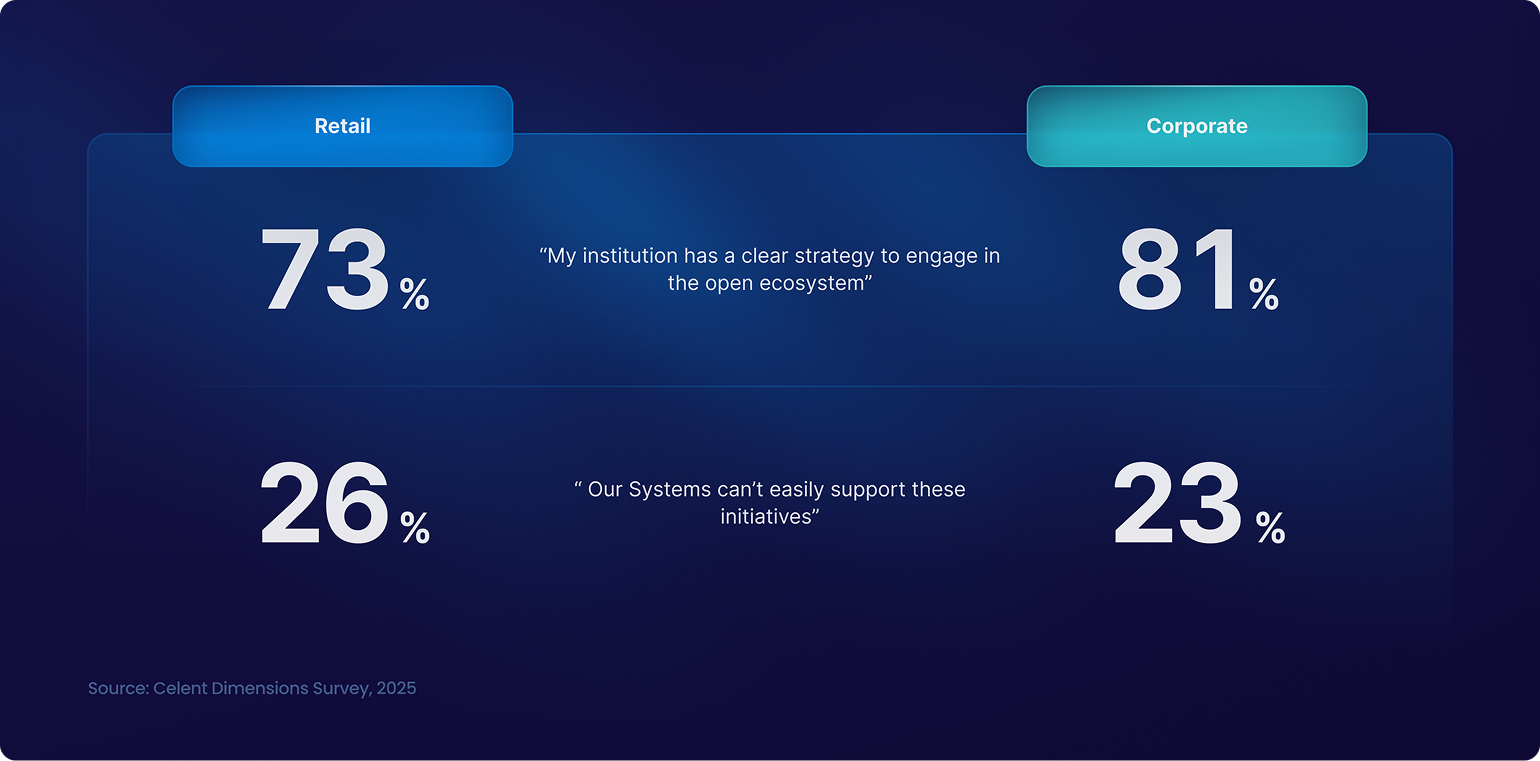

Intent alone is not enough to thrive in the platform economy. The true barrier is infrastructure. According to Celent’s Dimensions Survey 2025, most banks say they are ready for ecosystem banking, but their operating and technology models tell a different story.

The contrast between strategy and execution underscores the central challenge. Banks understand where they need to go, but their infrastructure often cannot take them there. Strategic intent outpaces system readiness, leaving even well-positioned institutions constrained by product-centric cores, fragmented data, and limited orchestration capabilities.

Siloed, product-centric core banking systems make it difficult to deliver customer obsession, partnership orchestration, and centralized governance at scale. Real transformation requires two foundational shifts that connect people, process, and platform.

- 1An operating model built for agility and scale Traditional operating models anchored in product silos fragment customer information, reinforce product-first thinking, and limit enterprise agility. Creating the customer-obsessed, partnership-driven organization needed to compete in the platform economy requires a structural shift: aligning around customer lifetime value and building enterprise-wide coordination capabilities. An agile operating model provides that foundation. It turns scale into coordinated execution while reducing risk, ensuring people, processes, and incentives focus on outcomes customers value. Just as importantly, it creates the flexibility to expand value-driven partnerships, enabling new partners to be integrated quickly and consistently without adding complexity. The result is a model that sustains transformation across the enterprise and extends seamlessly into partner ecosystems.

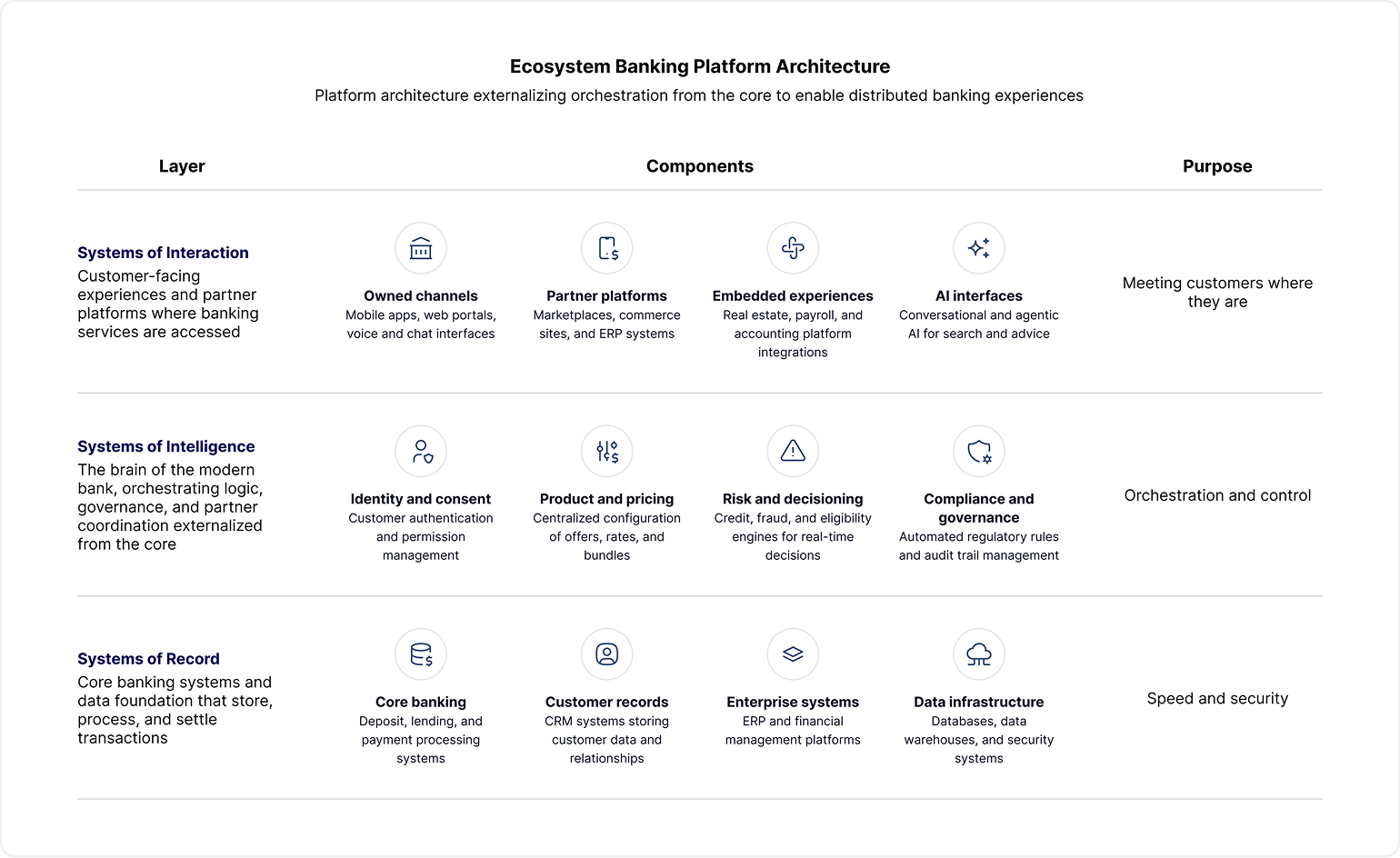

- 2Platform architecture built for governance and resilience Platform architecture is what makes this model real. Imagine a three-layer system: at the top, customer experiences and partner platforms; in the middle, an orchestration and control layer; and at the base, the bank’s core systems and data foundation. In the top layer, customers interact through apps, marketplaces, or partner platforms. Each experience calls the orchestration layer, which manages who the customer is, what they are allowed to do, and how the right product or decision should respond. In the bottom layer, the core banking systems record, settle, and safeguard every transaction. The orchestration layer connects these worlds — translating a customer’s intent into a secure, compliant financial action. Within this orchestration layer live the core capabilities that once sat deep inside the core: identity and consent, product and pricing logic, risk and decisioning engines, and the compliance rules that supervise them. Partner contracts, data, and evidence flow through the same layer, while routing, settlement, and performance reporting ensure that every transaction can be traced and governed. In this design, product and pricing are externalized from the core, data is unified, and compliance is automated at the point of action. The result is infrastructure that no longer slows innovation but orchestrates it — coordinating services, partners, and governance across every channel. This is how banks convert trust into transparency and scale into speed.

Orchestrate growth in platform economy

Download the latest Celent report to learn how to adapt your banking growth strategies for the modern banking landscape.

Delivering at Scale

No two banks take the same path towards transformation. Some are constrained by legacy product architectures, others by fragmented data or inconsistent governance. Yet the destination is shared: to move from understanding customers to being truly obsessed with creating value for them.

Thriving in the platform economy means evolving from product efficiency to ecosystem orchestration. This evolution requires new capabilities, new metrics, and a new mindset – one centered on customer-obsessed outcomes, seamless partner integration, and platform agility.

Charting the journey

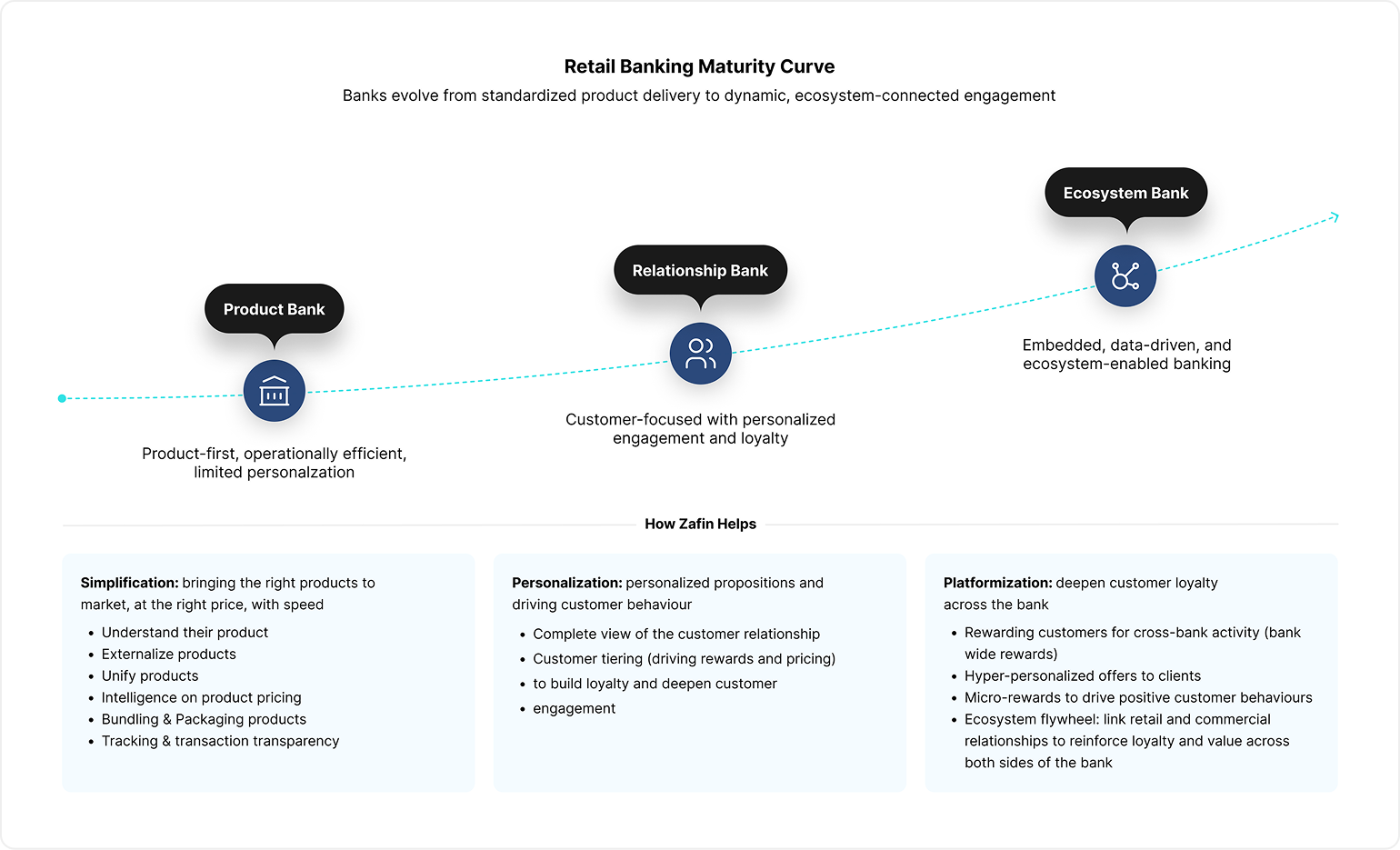

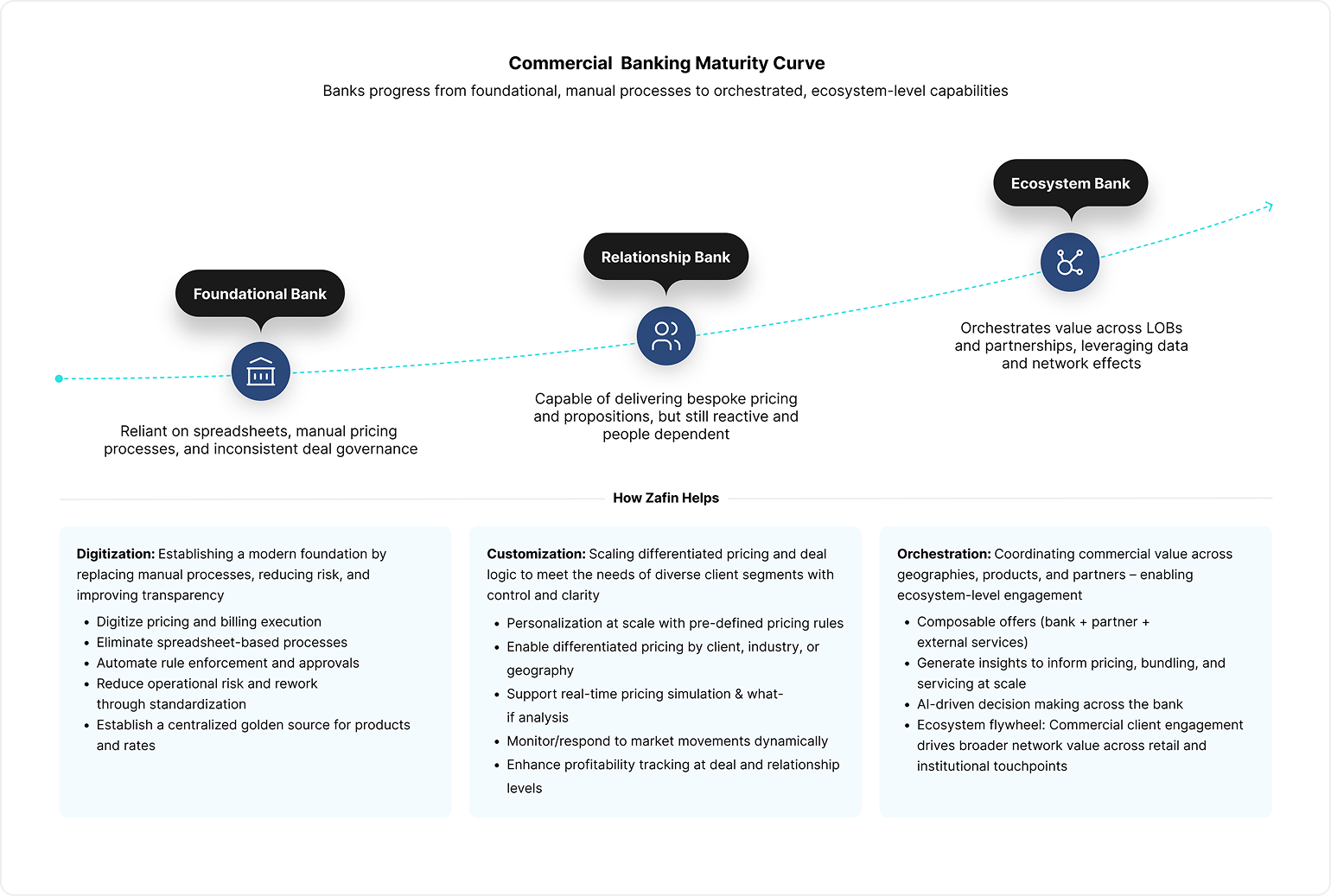

The Zafin Banking Maturity Curve offers a practical way to navigate this shift. It defines three stages of evolution – Product Bank, Relationship Bank, and Ecosystem Bank – each representing how deeply a bank connects its trust and scale to customer outcomes.

These stages describe a progression from efficiency to orchestration:

- Product bank: Operationally efficient and standardized, but siloed and limited in personalization.

- Relationship bank: Customer-aware, with increasing personalization, loyalty, and contextual relevance.

- Ecosystem bank: Embedded, data-driven, and capable of delivering value across platforms and partnerships.

This organizational progression also reflects a customer maturity lens: as banks advance from Product Bank to Ecosystem Bank, their relationship with customers deepens – from simply being aware of their needs, to engaged in serving them, to obsessed with anticipating and delivering on them.

Together, these dual lenses, organizational maturity and customer maturity, describe a single path: one where operational scale and customer relevance advance in tandem.

Across both retail and commercial banking, progress means translating trust and scale into personalization, orchestration and growth. The objective is not identical transformation but continuous advancement – turning awareness into engagement, and engagement into obsession.

Assessing your starting point

Every transformation begins with clarity about where you are today. The following diagnostic framework helps leaders assess readiness across four dimensions – customer experience, partnerships, agility and governance.

Each question highlights a capability that signals maturity on the journey from Product Bank to Ecosystem Bank.

Rather than a checklist, think of it as a reflection tool to identify strengths and gaps.

Ecosystem readiness assessment

Every transformation begins with clarity about where you are today. The following diagnostic framework helps leaders assess readiness across four dimensions – customer experience, partnerships, agility and governance.

Customer experience & personalization

- 1Do we deliver personalized pricing, offers, or rewards based on real-time customer behavior?

- 2Can customers access services seamlessly across channels without needing to repeat themselves or re-authenticate?

- 3Do we maintain a complete, enterprise-wide view of each customer’s relationship with the bank?

Partnership & ecosystem readiness

- 4Can we onboard new partners quickly through standardized APIs and governance frameworks?

- 5Do we expose core banking capabilities as callable services to third party platforms (offers, payments, accounts, issuing, credit decisioning), with safe test environments?

- 6Can we control distribution in real time across partners and channels (entitlements, rate limits, pause or exit switch) while keeping the customer experience seamless and consistent?

Platform & operating model agility

- 7Is our product, pricing, rewards, limits and eligibility logic centralized and configurable across all channels and partners from one place?

- 8Can we create, test and deploy new banking experiences without needing major code rewrites or infrastructure changes?

- 9Do we support modular product design and composable service orchestration with versioned APIs, self-serve documentation, and automated testing?

Governance & Compliance

- 10Are consent management, compliance, and risk controls implemented as services across all customer journeys and partner channels, with clear first- and second-line ownership?

- 11Can we produce performance reporting and audit evidence and enforce service level agreements for availability, latency, accuracy, settlement timing, funds availability, disputes, and recovery across both internal operations and external partners?

Interpreting the results

| Your Answers | Where You Are | What It Means |

|---|---|---|

| Mostly No | Product Bank | You’re optimized for internal efficiency but likely delivering fragmented customer experiences with limited personalization or ecosystem readiness. Your transformation should begin with unifying product, pricing, and data capabilities. |

| Mixed Yes/No | Relationship Bank | You’ve started the journey toward personalization and loyalty but still face structural limitations. Your next step is expanding coordination across journeys and integrating external value sources. |

| Mostly or All Yes | Ecosystem Bank | You’re operating as a platform-enabled, customer-obsessed, partner-ready bank. Your focus now should be scaling orchestration, enabling AI-driven decisioning, and embedding yourself deeply into customer ecosystems. |

Determining where to play

Not every bank will, or should, become a fully embedded ecosystem orchestrator overnight. Instead, strategic ambition should be defined based on where the institution can create the most differentiated value.

- Customer needs: Which outcomes (e.g. homeownership, wealth building, business growth) do you want to own or enable?

- Platform role: Will you primarily serve as the interface, the infrastructure, or both?

- Partnership strategy: Which ecosystems (retail, travel, commerce, health or others) best align to your brand and customer proposition?

The maturity curve provides options, not a one-size-fits-all path. A bank may pursue ecosystem banking in one domain, such as SME finance through ERP platforms, while continuing to build relationship depth in another, such as retail savings or wealth management. What matters is clarity of focus and intentional progression along the journey.

Advancing maturity

Progressing along the maturity curve requires alignment across people, process, and platform. Each dimension plays a role in moving the organization closer to ecosystem execution.

People and Culture

- Shift incentives from product performance to customer lifetime value

- Stand up cross-functional journey teams focused on end-to-end outcomes

- Introduce new orchestration roles responsible for managing third-party value delivery and measuring success through shared customer metrics

Process and Partnership

- Industrialize collaboration with partners. Standardize commercial terms, SLAs, consent, liability and onboarding to reduce friction

- Deliver personalized engagement, proactive, context-aware offers at key financial moments and rewards based on real-time behavior, wherever customers engage – across owned channels, partner platforms, and embedded journeys (e.g. accounting platforms, travel portals, commerce apps)

Platform and Technology

- Centralize product, pricing and relationship logic on a unified, configurable platform

- Embed consent, compliance, and transparency directly into the architecture

- Enable secure partner integration through prebuilt APIs, governance standards and measurable SLAs

Together, these elements turn strategic intent into execution at scale.

The platform as the engine of maturity

At its core, the orchestration platform centralizes the logic that governs pricing, product configuration, personalization, and relationship agreements. This becomes the execution backbone for how value is structured and delivered. By decoupling this logic from the core, the platform gives banks the capacity to move with speed, precision, and consistency through their transformation journey. It enables banks to meet customers where they are and deliver seamlessly across digital, human, and partner-driven channels. For Zafin, this is the foundation of maturity at scale. The platform turns trust and scale into governed, composable capability, accelerating progress from Customer Aware to Customer Obsessed. It transforms infrastructure into intelligence, relationships into relevance, and scale into sustainable growth.

The Moment of Choice

In a platform-led, AI-enabled economy, banks now stand at a crossroads. Waiting is still a choice — and its outcome is increasingly predictable. Margins continue to narrow as platforms set the terms of engagement. Brands fade into the background at the point of decision. Customer acquisition costs rise as regulatory expectations grow more complex. Banks remain valuable to the system, yet risk being commoditized within it.

Acting opens a different path. Trust and scale become levers for growth through partners. Customer outcomes, not products, define value. Revenue becomes more resilient, through bundles, dynamic pricing, and embedded distribution. And with orchestration and governance built into every layer, banks can move with speed and confidence at scale.

The banks that thrive will use their maturity as an advantage – transforming their architecture, culture and partnerships into engines of continuous relevance. They may not always own the experience, but they will own the foundation of it, serving as trusted infrastructure that powers value across the platform economy.

References and notes

References

Accenture. Banking in the Platform Economy; Reinventing Banking in the Ecosystem Era. BCG (Boston Consulting Group). Global Retail Banking: The Ecosystem Imperative; The Digital Banking Revolution. Celent (Oliver Wyman Group). Dimensions: Banking IT Pressures & Priorities 2025; Dimensions: IT Spending Forecasts by Domain 2025–2030. Deloitte. The Future of Financial Services: Open, Embedded, and Ecosystem-Driven; The Rise of Platform Banking. Ernst & Young (EY). NextWave Banking and Wealth Management; Open Banking and Embedded Finance Outlook. McKinsey & Company. The Future of Banks: A $20 Trillion Breakup Opportunity; The Changing Landscape for Banks; Value Creation in Banking. Oliver Wyman. The Next Generation of AI in Financial Services. World Economic Forum. The Rise of Embedded Finance in the Platform Economy. Cornerstone Advisors. Stemming the Deposit Outflow: The $2 Trillion Investing Opportunity for Banks and Credit Unions

All reports and research available via respective firm websites.

Company and Platform Sources

All company information was drawn from official websites, press releases, annual reports, investor materials, and 10-K filings.

Brands and Companies Referenced Adyen, Amazon, Apple Pay, Ariba, Bank of America, Betterment, BlackRock Aladdin, BNP Paribas, Brex, Chime, Citi, Commonwealth Bank of Australia, Coupa, DBS Bank, DoorDash, Evolve Bank, FIS, Fidelity, FedNow, Gojek, Goldman Sachs, Grab, HSBC, Jane, J.P. Morgan Chase, Kyriba, Lemonade, Mastercard, Mercado Libre, Microsoft Azure, mBank, NetSuite, Oracle, Paytm, PKO Bank Polski, Plaid, Policygenius, PrivatBank, QuickBooks, Ramp, Redfin, Revolut, Robinhood, SAP, SEPA, Shopify, Solarisbank, Square, Starbucks, Stripe, SWIFT, The Clearing House, TikTok, Toast, Tradeshift, Uber, Vanguard, Venmo, Visa, WeChat, Wise, Workday, Xero, Zafin, Zoho, Zoopla.

Media and Commentary Sources Reuters, Financial Times, Wired, MarketWatch, Finextra.

Industry reporting and news analysis on digital banking, AI, and embedded finance.

Zafin Research Zafin. Banking Maturity Curve Framework (Retail and Commercial); Ecosystem Banking Platform Architecture; Customer Outcome and Pricing Orchestration Model. Zafin.com.