The winter of 2021 brought weeks of icy, incorrigible weather to parts of the United States that usually bask in mild winters, and it tested the resiliency of families and businesses. The fragility of basic infrastructure in the face of a raging Mother Nature was shocking, but it shouldn’t be surprising. Extreme weather is no longer an aberration, at least, not according to the data. In 2020, there were 22 billion-dollar weather events which crippled cities and towns throughout the U.S. Over the last 20 years, no part of the country has escaped untouched.1

Predictions of continued extreme weather beg the question: what are businesses – and banks doing to ensure business continuity amid disasters of all kinds, whether natural or man-made?

The COVID-19 pandemic has prompted banks worldwide to fast-track some of their digital transformation roadmap, but the better strategy is to be planning for outages by building systems that operate uninterrupted in times of emergency. On premises banking systems cannot always do that when extreme conditions affect an entire region, as it recently did in Texas.

What are the pros and cons of on premises vs. off premises or cloud banking solutions?

On premises banking system affected by severe weather events

Whether it’s wildfires, hurricanes, flooding rains or blizzards, on-prem banking systems are not invincible to the elements. It may be impossible for bank employees to safely travel to the branch where computer hardware in located during a weather event. Equipment may be damaged or destroyed. If a bank has multiple branch locations within a tight radius, that loss may be especially magnified.

Demands on the back-up servers, even when located a safe distance away, can become overwhelming. Utilities may be down, and disaster-recovery processes to transition activity to secondary servers may take time to implement, further limiting banks from processing data in a timely, normal way.

In a nutshell, there is no fast path to normal operations for a bank when its on-prem hardware is affected, either temporarily or permanently. Restoring it, when possible, relies on critical suppliers and equipment that may be in short supply and overtaxed because of the disaster.Bank customers may lose access to in-person and online banking when on-premises systems go down – at the precise time they are most in need of assurance, peace of mind and financial security.

On premises vs. cloud banking: disaster recovery and beyond

Cloud banking, in which a third-party provider hosts and services a software solution, offers a number of compelling benefits to banks, with disaster recovery high on the list.

Cloud banking uninterrupted during local weather events

Many community banks and credit unions have multiple branches in a tight geographic area, multiplying the risk of data and equipment loss, even when it is distributed across different locations. Public cloud data centers, however, are spread out worldwide. They are built on geographic diversity, by design, to maintain continuity. Processing in the cloud continues uninterrupted because even if one data center is disrupted by a regional disaster, there are many others across the globe that remain unaffected.

Cloud banking – build for remote access

The COVID-19 pandemic has taught banks the necessity of being able to access systems remotely. Unlike on-premises solutions, cloud banking was designed for remote access from anywhere there’s an internet connection. Banks can operate virtually and seamlessly, whether bankers can get into the office or not, in dramatic contrast to on-premises solutions housed on hardware that might be underwater, frozen or simply impossible for employees to reach.

Cloud provider s- experts in security

Banks that consider migrating from an on-premises environment are sometimes hesitant to move to the cloud because they worry about the safety and control of their data.

Eve Aretaxis of ACI, says: “Risk-averse banks… are warming to the fact that the big cloud providers can spend more on security in a month than any bank could spend in a decade.” 2

Cloud providers have worked for years to develop and build their secure infrastructure, and they continue to invest. Their survival depends on maintaining an unyielding wall of protection for their clients.

Cloud solution – cuts expenses in infrastructure, frees them for innovation

In a natural disaster, the damage to on-premises hardware is costly. Equipment replacement can be slow. When systems are compromised, banks may be forced to use less-than-ideal, inefficient workarounds, including manual processing that must be reconciled later. Customer experience may also suffer.

Even without a natural disaster, on-premises banking solutions are expensive to buy and manage. Hardware needs to be robust and constantly upgraded. Software licenses can be costly and have inflexible, long-term contracts. Regular maintenance requires a strongIT staff to facilitate different business strategies and troubleshoot.

Off premises, cloud banking is already configured, tested, and maintained by the third-party provider. Updates are made quickly, vetted and pushed out to banks, without stress on the IT team. Cloud providers can also facilitate employee training and support, in many cases, as well.

Foster implementation – cloud banking is built for rapid launches

Adjusting to market conditions and opportunities can be tricky when you have an on-premises solution. Banks must lean on their own resources to build new variants, adjust workflows, test, re-test, and create manual processes to override legacy system limitations.It usually requires staff expertise pulled from different departments and away from daily responsibilities.

Cloud banking, on the other hand, can be instantly provisioned. Free of hard-coded constraints and antiquated processes, banks can take off running immediately after the agreement is signed without long lead times or straining already stretched resources.

Scalable – cloud banking for just-right delivery

Highly responsive to the ebbs and flows that come from consumer demand or through growth or acquisitions, off-prem cloud banking is adaptable, flexing up and down with the needs of the bank. With a cloud provider, banks are not held back by underpowered solutions, but instead, can easily add capacity and functionality without added infrastructure costs.

Cloud banking – system agnostic

Cloud solutions are typically system agnostic, so the off-prem choice can be integrated into their legacy platforms, regardless of the operating system they are using.

Cloud banking – roadmap to innovation, enhanced customer experience

In the summer of 2020, with the pandemic at its height, small business owners were applying for loans, and bank back offices were buckling under labor-intensive, time-sensitive applications.Some banks turned to cloud partners for the first time to automate processing, which sped up approvals and funding, a positive result for those most in need.

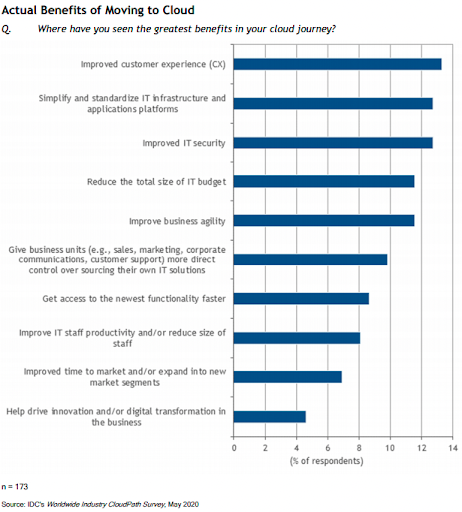

According to IDC‘s 2020 Worldwide Industry Cloudpath Survey, banks surveyed reported something surprising… they said moving to the cloud, viewed as more of an operational upgrade, also resulted in an improved customer experience.3

Furthermore, when banks choose to work with cloud-based providers, who are experts in the technology space, those providers become responsible for knowing and executing on best practices and cutting-edge innovations, relieving the bank from this burden.

Zafin’s cloud-native solutions – a win-win for bank and customer

Zafin’s cloud-native solutions were designed with the customer experience in mind. The goal? To center customers by providing relevant pricing and product strategies that strengthen their relationship with banks. Because Zafin’s solutions are cloud-native, they can be executed quickly outside a bank’s legacy core.

Zafin offers the rewards of core modernization without the risk, expense or long timelines. Browse all of our resources to read white papers, case studies, and articles on Zafin’s cloud-native solutions.

- https://www.climate.gov/news-features/blogs/beyond-data/2020-us-billion-dollar-weather-and-climate-disasters-historical

- https://www.statista.com/statistics/500458/worldwide-datacenter-and-it-sites/

- https://www.bankifi.com/blog/time-to-embrace-the-sme-customer

Founded in 2002, Zafin offers a SaaS product and pricing platform that simplifies core modernization for top banks worldwide. Our platform enables business users to work collaboratively to design and manage pricing, products, and packages, while technologists streamline core banking systems.

With Zafin, banks accelerate time to market for new products and offers while lowering the cost of change and achieving tangible business and risk outcomes. The Zafin platform increases business agility while enabling personalized pricing and dynamic responses to evolving customer and market needs.

Zafin is headquartered in Vancouver, Canada, with offices and customers around the globe including ING, CIBC, HSBC, Wells Fargo, PNC, and ANZ.