Key insights

- Regional banks face mounting pressure from renewed M&A activity, margin sensitivity, and heightened regulatory scrutiny, making operational precision more critical than ever.

- Resources, are more constrained for many regional banks, including both the capital and the personnel required to create and manage disclosures

- Disclosure management has become a business risk, not just a compliance task, as enforcement actions and consumer expectations raise the stakes for accuracy and transparency.

- Traditional disclosure processes are fragmented and manual, slowing product launches, creating version confusion, and limiting traceability and auditability across channels and customers.

- A governed, component-based approach modernizes disclosures, centralizing content, enabling structured approvals, and linking changes directly to products, pricing, and regulations.

- The result is faster execution with demonstrable control, empowering mid-market banks to grow confidently while strengthening compliance and audit readiness.

U.S. Regional banks are navigating a period of heightened scrutiny and rapid change. Competitive pressure is climbing, regulatory expectations are rising, and customers are demanding clarity and speed. In this environment, something often considered administrative like disclosures has become central to growth, compliance, and operational efficiency.

Disclosures has transcended its “back office” status to become a strategic capability that can accelerate product launches, reduce risk, and build customer trust.

1. Macro Outlook: Why Regional Banks Are Under Pressure

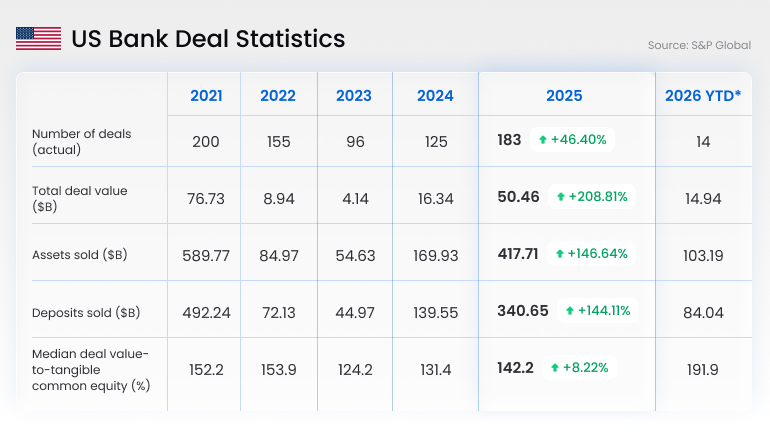

In the past few years, banking consolidation reached a decade-plus low. In 2023, only 98 U.S. bank M&A deals were announced.1 That trend reversed partway through 2024, and in 2025, 179 transactions with $190 billion in deal value (a 129% increase from 2024) were disclosed2 , pointing to a renewed consolidation cycle. At the same time, the regulatory environment has become more predictable. In March 2025, the FDIC proposed rescinding its 2024 merger policy statement, citing the uncertainty it introduced into the approval process. Two months later, in May 2025, the OCC adopted an interim final rule restoring streamlined and expedited merger review procedures. These moves didn’t create consolidation, but they did reduce friction. This shift signals that regional banks must position themselves to compete and scale.

Simultaneously, performance realities are stark. According to the FDIC, 6.7% of banks were unprofitable in 2024 3 , with earnings highly sensitive to funding costs and expense growth. Inefficiencies in operations or compliance can quickly erode margins.

Regulatory and consumer scrutiny adds to the pressure. High-profile enforcement actions highlighted the risks associated with inadequate disclosures. For example, the Federal Reserve assessed a $44 million penalty against Green Dot for insufficient fee disclosure 4. These events emphasize that disclosure accuracy and completeness are not just compliance boxes to check, they are business risks with financial consequences.

In this environment, banks must do more than maintain compliance. They must be able to execute confidently, accurately, and at speed.

2. Trends Banks Are Experiencing and Why They Create Urgency

Customers expect seamless digital experiences, transparent pricing, and relevant offers. And increasingly, they compare their bank’s responsiveness to the agility of fintechs and large national institutions. Regional banks want to deliver digital speed and personalization, but internal capacity often falls short.

Many institutions describe being resource-constrained, especially in compliance teams that are tasked with multiple responsibilities and without major technological enablement. In fact, 60% of community and regional banks mentioned being resource constrained, specifically in compliance and product teams that have multiple responsibilities without major technological enablement. This constraint shows up in delivery speed. What should be a matter of weeks (updating a disclosure or launching a new product) can take months.

Slow execution has real business impact. Delayed product launches weaken competitive response and can leave meaningful revenue on the table. Fragmented documentation practices elevate compliance risk. The need is not just to move faster, but to move with provable control and auditability.

3. What’s Broken: Disclosure Process Challenges

Across the industry, managing disclosures remains fragmented. Banks store content in disparate systems such as core platforms, shared drives, and cloud document repositories. Responsibility for content is often scattered among compliance, product, legal, and operations teams. In this setup, basic questions become hard to answer:

- Which version of a disclosure is current?

- Where is it deployed across channels?

- What changed, when, and why?

- Who approved the change?

Zafin Disclosures powers the end-to-end disclosure lifecycle

Automated, compliant, and customer-aware — Zafin brings structure and scale to every step of the disclosure journey

New product, offer, pricing or regulatory change initiates disclosure need

- Disclosures automatically initiate when product or offer changes

- Product, pricing and offer data from Zafin flows directly into disclosure logic

- Legacy documents are quickly converted into structured content using AI-powered ingestion

- Create content using reusable, modular, pre-approved components

- Grouped into disclosure sets — complete, approved packages for a given use case (e.g., product disclosures, offer disclosures, rate sheets, account agreements, website legal content)

- Teams can tag content to regulations, ensuring traceability from the start

Approvals are routed through product, marketing, legal and compliance workflows

- Every change is tracked with full version control and audit logs

- Workflows can be managed by Zafin (no-code, rules-based) or integrated with 3rd-party services (e.g., Adobe Workfront)

- Approval paths align to product type, regulation, or jurisdiction

Disclosures are formatted and delivered across all channels

- Approved disclosure sets are bundled and delivered to bank via API

- Zafin supports PDF, HTML, and JSON outputs

- Design and generate PDF templates or connect with existing tools

Track what was shown, when, and to whom — down to the customer level

- Every disclosure shown to a customer is timestamped and linked to the exact version

- Capture customer consent and surface it later if needed

- Servicing teams can instantly retrieve what was shown and agreed to, reducing resolution time and risk

Some banks operate with manual approval steps. Documents circulate via email with no centralized workflow or audit trail. Version control can depend on file naming conventions rather than governance processes.

Equally concerning is traceability. Even if a final version is archived, many banks cannot reliably demonstrate to the regulators during audit exams which specific disclosure was presented to a given customer, through which channel, and under which product configuration. Several surveyed bankers noted that final disclosure versions are often stored on local hard drives, or Google Drives. Under increased supervisory focus, this gap exposes institutions to enforcement risk.

In addition to being a compliance headache, it also slows execution and dilutes confidence in the bank’s controls.

The pain point obviously is the time it takes to work on disclosures. We are resource-constrained because we only have so many people to do everything,” said a VP of Risk at a midwest community bank.

“Currently, it’s just manual emails between teams to update disclosures,” reported a compliance lead at a community bank in Arkansas.

“It costs more to correct the legal implications if something goes wrong than invest in technology to prevent it,” observed a former executive at a regional bank on the East Coast.

These voices reflect a broader industry challenge: disclosure management is inefficient, risky, and often invisible until something goes wrong.

4. The Right Framework: Governed, Component-Based Disclosure Management

Rather than managing disclosure content as static documents scattered across folders, leading banks are adopting a structured, governed approach that centralizes and modularizes disclosure content. Modern disclosure management treats each clause or element as a reusable component linked to underlying product definitions, pricing logic, regulatory references, and customer context.

Many institutions create a new disclosure for each product or variation, even within the same product family. Over time, this results in hundreds or thousands of documents, often with significant overlap. In practice, a large portion of this content is repeated, with teams copying and pasting from prior versions. This increases the likelihood of inconsistencies, outdated language, and missed updates.

A modern approach begins with rationalization. Existing disclosures are ingested, analyzed, and broken down into standardized, pre-approved components. This creates a clean, controlled foundation, reducing duplication and establishing a single source of truth before new changes are introduced.

From that foundation, the model delivers three critical outcomes that address the capacity and risk challenges regional banks face:

Rationalized and controlled foundation

By consolidating overlapping disclosures into reusable components, banks significantly reduce the volume of content they need to manage. Standardized, pre-approved clauses replace duplicated language across documents, lowering both administrative burden and the risk of inconsistency. Instead of maintaining hundreds of loosely related files, teams operate from a governed library of components that can be confidently reused across products and channels.

Controlled change management

When a fee changes, or a regulatory requirement shifts, the system can automatically identify which disclosure components are impacted. This eliminates manual search and reduces the likelihood of missing required updates.

Structured workflow and governance

Role-based approval workflows and a complete version history provide clarity about who made changes, when, and why. Full audit trails and side-by-side comparisons replace email chains and file naming conventions with structured governance that supports accountability and audit readiness.

Customer-level traceability

Disclosures are tied directly to specific products, channels, and individual customer interactions. This creates a defensible compliance record of what was presented and accepted. It also increases confidence in customer communications across digital and offline touchpoints. In a world where hyper-personalization and the ability to provide 1:1 personalized offers to the consumer exists, traceability is even more important.

This is where Zafin’s Disclosures capability becomes relevant for regional banks that want to operationalize this modern framework. Our solution centralizes banking disclosures into a dynamic modular library, enabling banks to build and distribute disclosures at the product, offer, and customer levels with greater speed, consistency, and accuracy. The platform delivers:

- AI-powered assembly and migration to turn legacy disclosure files into structured, reusable components.

- Configurable, rule-based workflows that support multi-level approvals and role-based permissions.

- Full audit history and traceability, including version, timestamp, and approval records.

- Integration with MarTech and CRM systems for consistent delivery across channels such as email, SMS, mobile app, and web.

Connecting disclosures directly to underlying product attributes and regulatory tags helps banks respond quickly when rates, fees, or rules change, and enables them to maintain compliance with demonstrable evidence across every customer segment.

This approach supports faster product execution while reducing compliance risk and operational drag, a combination that is especially valuable for regional institutions with limited internal capacity.

Enabling Growth Without Compromise

The pressures facing regional banks are unlikely to diminish soon. Funding costs, customer expectations, and competitive intensity will continue to evolve. In this context, disclosure management is a foundational capability that enables faster product launches, better risk management, and more transparent customer interactions.

By adopting a governed, component-based approach to disclosure management, regional banks position themselves to:

- Shorten time to market for new products and offers.

- Improve operational efficiency by reducing manual effort and rework.

- Strengthen compliance evidence with audit-ready workflows and traceability.

- Support personalized customer communications that build trust.

Zafin’s Disclosures transforms what used to be a bottleneck into a competitive capability. It encourages a mindset shift from managing documents to managing controlled content, aligned with product strategy, compliance strategy, and customer engagement.

Ready to elevate the speed, compliance and trust of your disclosures? Talk to one of our experts today.

Ultimately, effective disclosure management enables regional banks to run their operations with confidence, deliver customer value more rapidly, and minimize business risk at a time when all three matter more than ever.

Sources:

- https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/2/bank-m-a-2024-deal-tracker-10-deals-announced-in-january-80319065

- https://www.mckinsey.com/capabilities/m-and-a/our-insights/financial-services-m-and-a-bounces-back-with-scale-and-capabilities-at-the-center

- https://www.fdic.gov/news/speeches/2025/fdic-quarterly-banking-profile-fourth-quarter-2024

- https://www.federalreserve.gov/newsevents/pressreleases/enforcement20240719b.htm