Executive summary

CMOs are under increasing pressure to prove that marketing drives measurable growth. Yet when it comes to offers, the highest-cost and highest-volume lever in retail banking, most cannot answer a simple question: What value did we actually generate for what we spent?

Offer performance remains opaque because execution, fulfillment, and measurement are fragmented across teams and systems. Marketing can launch campaigns but often cannot verify whether offers were executed correctly, fulfilled as intended or reconciled to actual financial outcomes.

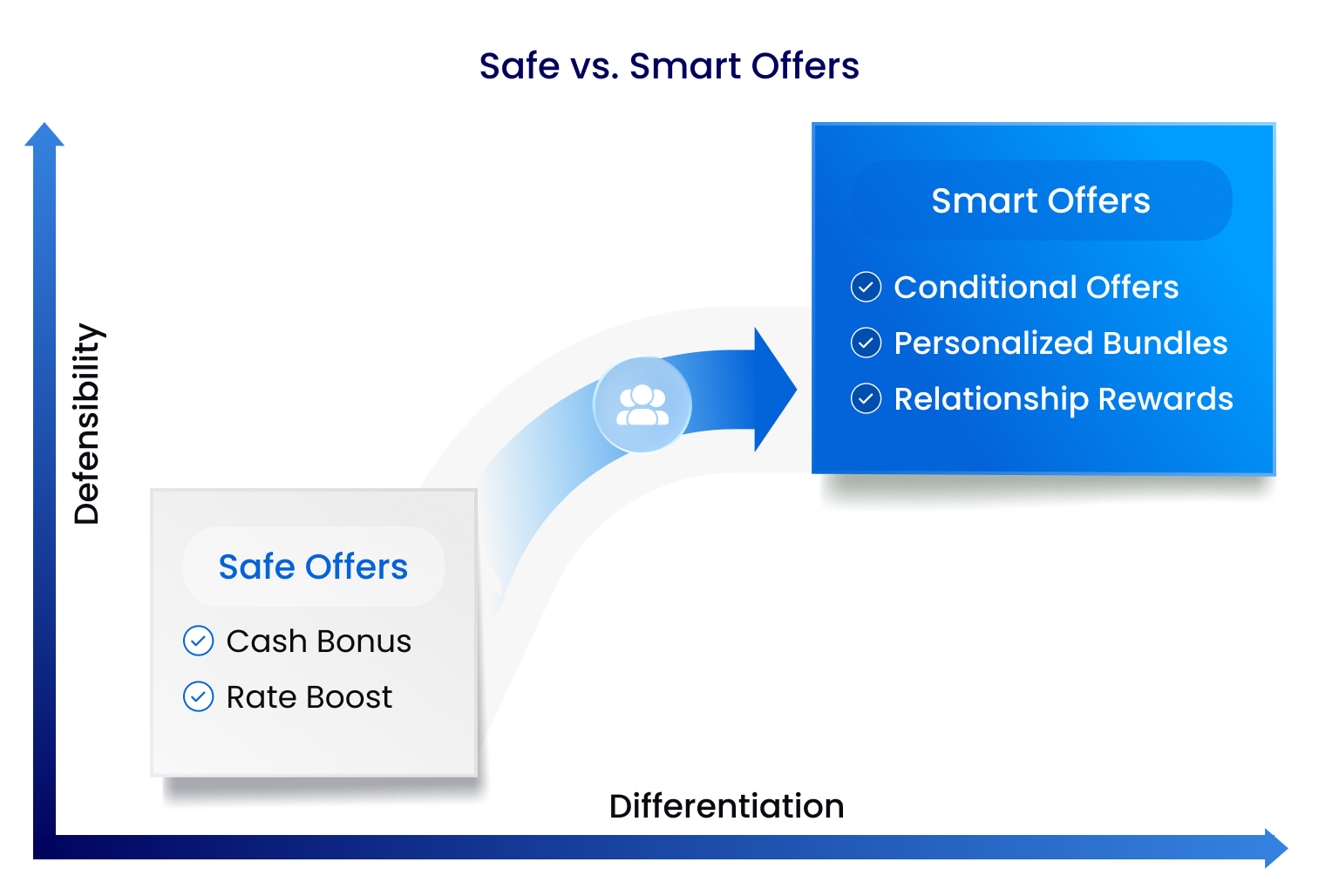

The result is predictable. CMOs fall back on blunt incentives like rate boosts and cash bonuses. Not because they lack ambition, but because these offers are easier to execute, justify, and defend internally.

Fixing this requires a shift in mindset: offers must be managed as an end-to-end governed lifecycle, from initiation through execution, fulfillment and financial reconciliation.

The banks that close this gap enable marketing to defend ROI with finance-grade evidence because outcomes are derived from what was executed and fulfilled, not inferred from engagement metrics.

The CMO reality check

Digital challengers are pushing banks toward faster cycles, tighter targeting, and always-on offers. But most institutions lack the infrastructure to ensure offers are executed consistently, fulfilled correctly, and measured reliably.

When something breaks (a missed reward, an incorrect fee waiver, an inconsistent experience across channels), the impact is immediate. Frontline teams absorb the pressure, and escalation can quickly reach senior leadership or even create regulatory exposure.

Marketing owns the promise. But it does not fully control the outcome.

And that gap between promise and delivery is where value is lost.

Why Banks Can’t Innovate Beyond Rate Boosts and Cash Bonuses

Banks don’t default to simple offers because they perform better. They default to what can be executed consistently and defended internally.

Speed constraints: More sophisticated and innovative offers (like multi-product, tiered, or beyond banking) take too long to design, approve, and configure across fragmented systems.

Execution risk: The more personalized or conditional the offer, the higher the risk of misapplication, complaints, and costly remediation.

Measurement weakness: If ROI can’t be proven, investment decisions default to what is easiest to justify and forecast — reinforcing reliance on cash and rate incentives. Marketing must strive to consistently prove credibility, so their initiatives receive adequate funding and attention.

The result is a cycle where simple, blunt incentives dominate because they are safer, not better.

Banks are not optimizing for what drives value. They are optimizing for what they can confidently execute and defend.

The ROI Visibility Problem

When budgets are reviewed, CMOs face questions that are difficult to answer with confidence:

- What did we actually spend, including overpayments, overlaps, and manual exceptions?

- How much of the growth was truly driven by the offer, versus customers who would have acted anyway?

- Where did the impact land: product P&L, relationship profitability, retention?

- Did we deliver what we promised, consistently, across channels?

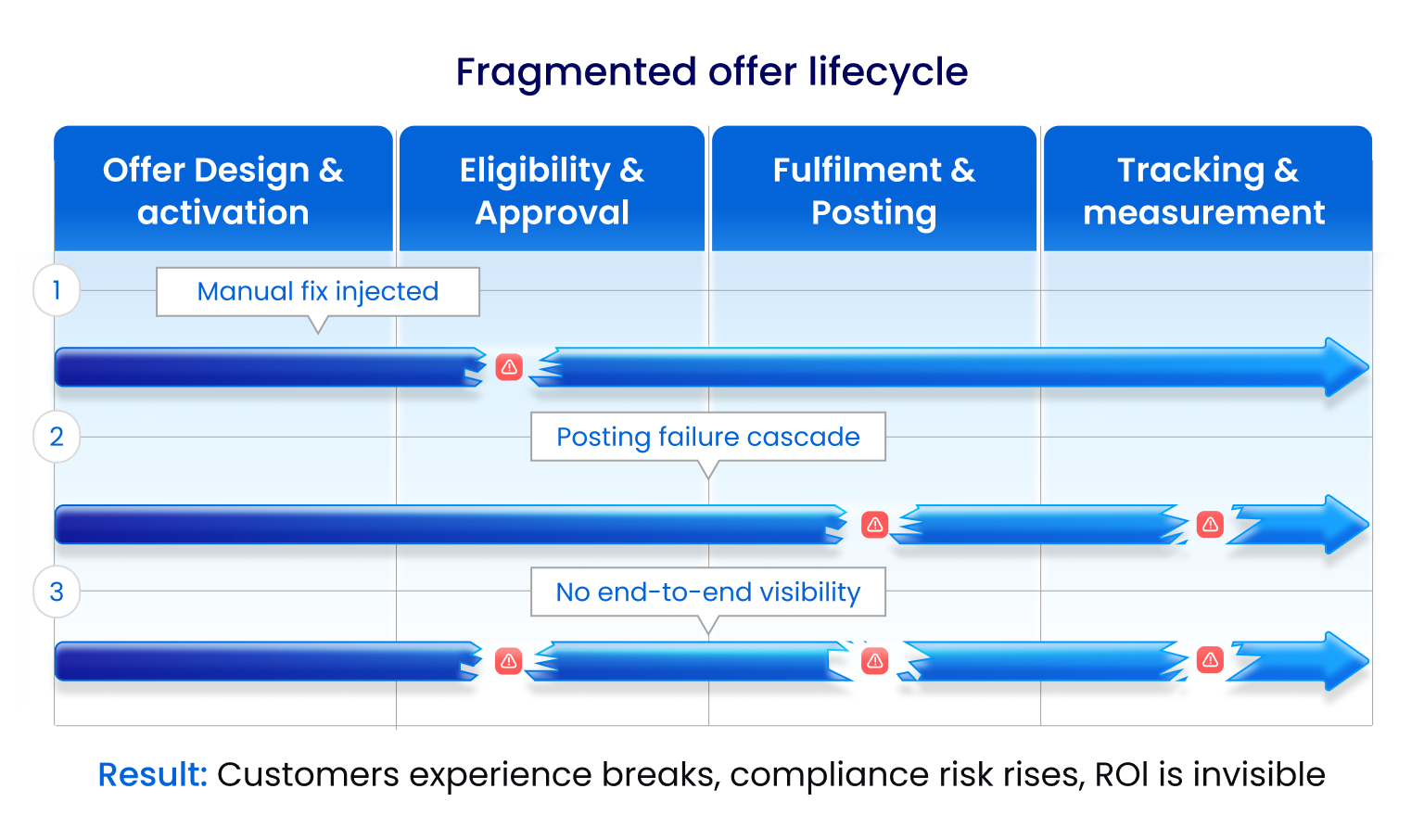

Most banks cannot answer these definitively because the problem is structural.

The offer lifecycle is fragmented:

- Exposure sits in MarTech systems

- Eligibility lives in rules engines

- Fulfillment happens in the cores and ledgers

- Reporting lives in BI tools

Marketing sees engagement and enrollment. Finance sees financial postings. Neither sees the full lifecycle.

Attribution often stops at clicks or acceptances, even when fulfillment fails. Audit trails are incomplete. Offer versions and decisions are difficult to trace.

Offers are treated as marketing commitments. But they are executed like distributed IT configurations.

Without end-to-end control and traceability, ROI becomes a debate. This can frame marketing as just a cost center instead of a revenue generator.

What “good” looks like

Leading banks are shifting from campaign reporting to controlled offer performance management.

They treat offers as governed financial events, not campaign artifacts.

This means:

- A single, end-to-end view of the offer lifecycle: who qualified, who enrolled, who fulfilled, and where breakdowns occurred

- Controlled fulfillment: tracking benefits and rewards through completion, reversals, and exceptions

- Decision-grade analytics: measuring true impact, incrementality, and performance across cohorts

In this model, performance is based on what was actually delivered, not what was intended or inferred.

How leading banks close the offer ROI gap

Closing the gap requires infrastructure that connects promise to outcome.

That means:

- Owning the full offer lifecycle, from definition and eligibility through fulfillment and financial impact

- Measuring based on delivery, not engagement proxies

- Creating a single source of truth for cost, performance, and exceptions

- Reconciling outcomes in finance terms, not marketing metrics

- Maintaining audit-grade transparency across approvals, versions, and execution

When these controls are in place, CMOs can walk into budget conversations with confidence, backed by evidence instead of assumptions.

Zafin’s Offer Management solution provides this control layer by owning eligibility, execution, fulfillment, reconciliation, and analytics into an end-to-end governed, auditable system of record. Zafin’s control layer is already helping large banks around the world expand the number of offers they launch, how quickly they launch and fulfill them, see clear ROI, and prove them with confidence.

Because if offers are not executed and fulfilled correctly, they cannot be proven and ROI becomes guesswork.